Housing Permits, Starts, Recessions and the Economy

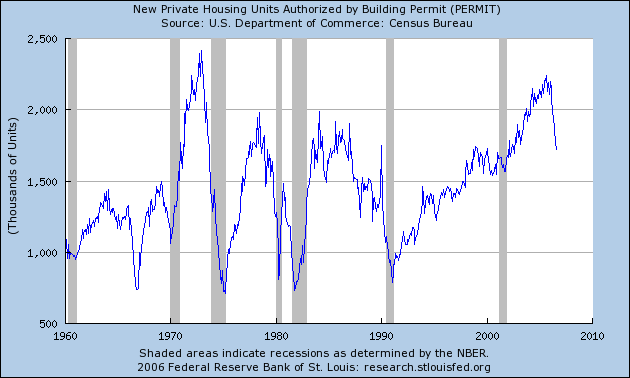

Again, Professor James Hamilton posts some very interesting data that doesn’t bode well for the economy. The first graph is of housing permits

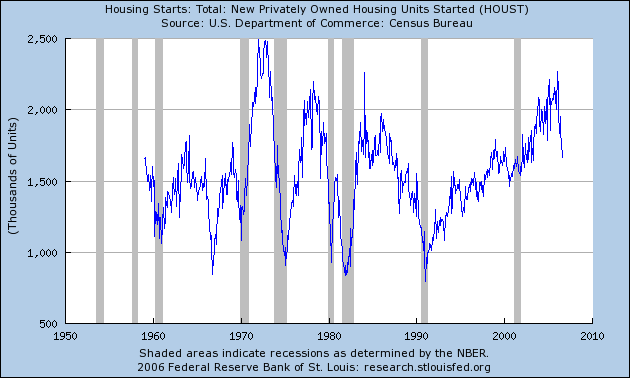

The next graph is of housing starts.

Now I haven’t done any statistical analysis, but just by “eyeballing” the data it looks very much like housing permits and starts are somwhate correlated with the business cycle. This makes some sense because we can tell the following reasonable “story” about why this should be the case. When housing permits and stats fall that is an indicator that housing prices are falling or about to fall. This decrease in housing prices results in a (negative) wealth effect for many people. That is they cannot use the equity in their house for consumption spending. This contraction in consumer spending (consumer spending is a large component of the economy) could very well be large enough to send the economy into recession. Now this isn’t the only variable at work here which is why we have seen other declines in housing permits and starts without recessions. Still, when there is a recession, it does look very much like it is associated with a decline in housing starts and permits. The big question is how strong is the relationship in the other direction? That is, when housing permits and starts decline percipitously, how likely does that make a recession? For example, there is a large decline in housing starts in the late 1960’s that is not associated with a recession. Also around 1994 or so there was another decline that was as large as the decline around 1960 that also is not associated with a recession.

Prof. Hamilton’s take on the data,

It is hard to find an example of a decline of this magnitude that wasn’t associated with a recession. We saw something comparable in 1987-88, though my view is that the 1987-88 housing downturn left the economy weak enough that the oil shock of 1990 then tipped us into a recession. For a really convincing example of declines of this year’s magnitude that did not produce a recession, I think you have to go back 40 years to 1966-67.

Translation: this decline is not good. It may not mean a recession, but that outcome is looking less and less likely (well at least that is my take on his comments).

Then there is Calculated Risk’s prediction about the jobloss implications of this kind of decline (that also becomes stable and does not continue to decline for the next several months). The bad news, 600,000 private construction jobs lost. The good news…uhhhmmm there really isn’t any. The Big Picture also has some information on the potential for loan delinquencies. Here are some of the disturbing statistics,

- 70% of borrowers who took out pay-option ARMS in the past year have loan balances larger than their initial loan.

- Homeowners face higher payments as mortgages are reset. Generally, monthly payments rise between $200 and $500 depending on the size of the mortgage.

- According to Reality Trac, August foreclosures were up 23% over July and 53% over a year ago.

President Bush keeps saying that the economy is strong and that the tax cuts have done their job. The problem is, for how much longer is this going to be true and how hard is the landing going to be? My own view is that the notion of a “soft landing” is quite unlikely.

Okay, not such great economic news for the future. What are we to do? Is the government to do something?

The bad news, 600,000 private construction jobs lost.

Yeah, but those jobs are filled by illegal immigrants anyway, so maybe they will go home?

/snark

The other side is that you can see fall offs one in the 60’s, one in the 70’s and twice in the 80’s that were about the same size that didn’t lead to a recession. Further, four of the five previous drop offs associated with a recession showed drop offs that took the number of permits to well under a million (and the case in the 60’s that took it to under a million, but with no accompanying recession). The oddball was the last recession where housing starts went down, but it was well within the normal rise and fall.

So what was different about the last recession that didn’t see the same tanking of housing permits? In the last recession the feds tried to control things by dramatically lowering interest rates. This helped to keep the housing market up because the costs to own a house in real terms was lower. Now look where housing permits start to fall off. It coincides with the rise of interest rates which means that the real cost of buying a house goes up.

It could be that the market for new homes is less than 2+ million per year. We aren’t experiencing a baby boom entering the home buying market to drive a larger demand. We may be seeing a correction to the housing market responding to the straight forward economics of pricing. When the real cost of housing was low (because of low interest rates) the demand for the good went up (if this is a surprise, please review chapter one of you economic text book). When the real cost of housing went up, demand for the good went down (I believe this is also covered in chapter one).

I’m not saying that this might not be the canary in the coal mine of a recession. I am saying that this data doesn’t prove it and that there are alternate explanations that adequately explain what we are seeing that don’t necessarily point to a recession. I do hope the Fed would bring the interest rate down a half a point, but so far they haven’t asked for my opinion.

“This decrease in housing prices results in a (negative) wealth effect for many people. That is they cannot use the equity in their house for consumption spendingâ€

I believe most people don’t take out a second mortgage on their houses. So this effect on the economy would be small. Price of someone house usually only affect them when they buy, sell and pay taxes.

YAJ,

I think you are deliberately burying your head in the sand. Oil/gasoline prices, while lower, are still pretty high relatively speaking. Interest rates are higher. Lots of people have ARMs that are about to take a significant step upwards, and housing starts/permits have dropped. Car sales are off, especially for things like SUVs and the like which is hurting, badly in GMs case, the auto industry. Even tax receipts have been decreasing. Exactly how much more data do you need before you start to come around to the idea that the economy is getting weaker not stronger?

Or as Keynes once said, “When the facts change, I change my mind – what do you do sir?”

There was a wave of refinancing when interest rates were low. If people opted for low payment ARMs and didn’t lock in a fixed rate now they face having significantly higher payments. So, I don’t see your argument being very persuasive in this case.

Steve,

What you have repeated several times is that interest rates are up. You say it explicitly. You say it as causes to the effect (new homes and car sales are down) on things whose sales are dependant on interest rates (few people pay cash to buy their home or car). You say it as implicit in a problem (ARM’s are coming do, why is that a problem, because interest rates are up). And certainly a component of the car sales declines, especially the SUV’s could be the gas prices. Which you note are going down.

As far as tax receipts going down, they have been up year on year for 10 out of the 11 previous months. The one exception is a very slight decline in one month. That of course is at least partially offset by a record September as corporate taxes coming due in September 15 set an all time high.

If you are arguing that the fed should reduce the interest rates, I am with you. But what I don’t see is that you have made a case that the economy is about to go over a cliff. I think you have made a case that the fed has interest rates to high and they should back off a bit. It could be that the economy is about to go off the cliff, but it could also be that interest rates are just a bit to high.

Taking the housing data, we see that housing permits are off by about 500K. Similar to the four “false warnings” of a recession in the 60’s, 70’s and 80’s. But what you haven’t shown is that the number of housing starts is below what the economy needs. Where we were at was an unusually high number of housing starts. Given that the average in the 70’s, 80’s and 90’s looks to be less than 1.5M per year, you need to explain to me why housing going to 1.75M per year is not the market just correcting for what had been a relatively low priced good due to low interest rates. Now that interest rates are up, it is not surprising that the market would correct back.

You are pointing to a weather vane and predicting a storm. While you may be right, what I am pointing out is that another factor may be influencing the weather vane (e.g. an unshielded MRI).

Do you really have that much trouble seeing that an alternate issue (higher interest rates) could be causing all the signs you are pointing to as indicative of a tanking economy?

Steve

Take a chill pill. YAJ and I are not saying that we shouldn’t keep an eye on the economy or even which way the economy is going. It just those so call hard line indicators that you seem to want to use are not as great of indicators as you are letting on or the implication of them. You seem to be grasping for data to support your furlong conclusion about like those conspiracy theorist type.

YAJ,

Interest rates are not the only driver here. Car and SUV sales are also down, not just because of interest rates, but also the higher oil/gasoline prices. And yes, interest rates that are too high can trigger a recession. Seriously, look at 1980, there is one example right there. The one shortly after 1990 has also been blamed on monetary policy as well.

As for taxes, yes I’m quite aware of the data as I’m the one who posted that picture. The point is that all the data is starting to point in one direction: an economic slow down. Most of the people who deal with this data also think this is the case as well.

Wow, that is an impressive strawman. I have never said it is about to go over a cliff. Most predictions indicate that 2006 will remain positive and the slow down will come in 2007 maybe 2008. The big question is how much things will slow down. I’ve written that in the opening post, and in my comment to you I claimed the economy is getting weaker, not about to go over a cliff.

I’ve already noted that the decline in housing starts isn’t a perfect indicator yet you imply I have claimed it is perfect indicator. Also, look at the graph and show me more than one drop of this magnitude that isn’t associated with a recession. And yes, we were at a point where the number of starts and permits was very high…just as with the recessions in mid 70’s, the 1980, and early 90s.

Now that is a gross mis-statement. There isn’t just a weather vane, but the high oil prices, which now considerably lower, but still pretty high. Add on the interest rates and lack-luster performance in the payroll survey and things sure as Hell don’t look like sunshine and daisies. It may not be a tornado or hurricane, but some rain and possible high winds definitely strike me as a real possibility…to use your metaphor.

Once again, higher interest rates, all by themselves, can tank the economy. See this post by James Hamilton that has a nice graph shwoing the relationship. And please don’t respond with the obvious strawman that I’m claim any and all recession have and always will be caused by interest rates.

Wayne,

That was stupid. I have posted lots of data so far, and you and YAJ have posted precisely nothing in terms of data, but I’m the conspiracy theorist.

Actually I tried to point out four of them. The current decline is about 500K.

So in the 60’s, we had what looks to me to be about 1.3M to 0.75M.

In the late 70’s, there was a fall from just under 2M to about 1.5M, it then went up 250K and about a year later went down to about 0.8M.

About 1984, it again went from just under 2M to 1.5M.

In about 1986, it went from about 1.8M to about 1.3M

So there are four drops not associated with reccessions (maybe the late 70’s one, but the drop seems to be quite a bit ahead of the recession and half the drop was made up before the recession).

Do you understand my point about a market “norm” as to the number of new houses the economy would demand, all other things being equal? The norm for this market looks to be a bit below 1.5M houses per year. The times associated with the market above 1.5M seem to be balanced with time below. This makes sense as buying a home is often something that can be postponed. Pent up demand is created so the lows get balanced with highs. But looking bachk over the last 10 years, we have been seeing housing permit well above the 1.5M. The last “correction” should have been during the 2001 recession, but there wasn’t one. I theorize that this could be due to the normal market being distorted by historically low interest rates.

So when you point to this as data that “doesn’t bode well for the economy”, “could very well be large enough to send the economy into recession”, “It may not mean a recession, but that outcome is looking lees and less likely”, and “how hard is the landing going to be? My own view is that the notion of a ‘soft landing’ is quite unlikely”, I am merely pointing out that there is another equally rational explination. That the market is just getting back into balance. You don’t seem to be able to refute or even address the issue directly. You just continue to insist that the data you show indicates we are likely heading into a recession. You do not convince me. Show me that the data is more likely to indicate a recession than something else. There are five cases where a drop in permits like this was immediately followed by a recession (1970, mid-70’s, 1980, 1981 and 1990). There is one case where the recession was not pre-saged by a dramtic drop in permits. There are four cases where a drop of equal magnitude didn’t presage a recession (as I listed above). I’m sorry if you are offended, but I don’t see that as evidence that would say we are heading into a recession. Just taking the odds, its 5 to 4 we are, but other factors may be in play.

I agree that monetary policy can push an economy into a recession. Leaving the interest rates even isn’t what I would do, but that at least argues that someone is recognizing that raising interest rates isn’t the right thing.

You posted and built your argument that “doesn’t bode well for the economy”, “could very well be large enough to send the economy into recession”, “It may not mean a recession, but that outcome is looking lees and less likely”, and “how hard is the landing going to be? My own view is that the notion of a ‘soft landing’ is quite unlikely” on these graphs and what they fortell. We are just going to have to agree to disagree because I am not reading the same things into the tea leaves.

I’ll leave you with the following cheap shot.

‘things sure as Hell don’t look like sunshine and daisies.’

‘Wow, that is an impressive strawman. ‘

You are making the same sort of strawman arguments. Show me where I said anything remotely like this was a sign the economy was all “sunshine and daises”. I think your statements come a lot closer to “the economy is tanking” than any of mine comes to “sunshine and daises”. Goose-Gander-Sauce.

Steve

It is not your data that I have a problem with. It is how you attempt to use it. YAJ have pointed out many flaws in your analyses. Conspiracy theorist tends to have a line of thought and analyze facts in a way to support it and ignores any other explanation.

For example, saying Bush blew up the WTC and that jet fuel doesn’t burn hot enough to melt steel as proof. If anyone tries to explain the flaw of the jet fuel argument, the theorist calls him or her stupid and keeps repeating that Bush did too blow up WTC.

In logarithmically the change now is actually greater than back in 1984 going from peak to trough (assuming that we are looking at the trough for 2006).

This one, logarithmically is a bit bigger than the current decline, so you have one here.

As for the late 70’s that one is debatable since the decline you are talking about could be viewed as part of a larger decline. Basically, the series grew for two more months before continuing its downward trend.

So overall, I’d say you have 2.5 examples (half credit for 1970). And all this hinges on the decline bottoming out right now and staying pretty level. In the next couple of months well get a better picture and I still see no reason not to think that the economy is getting weaker. This decline in the housing market is problematic. As Edward Leamer has noted, 9 out of 10 recessions are usually preceded to some degree by a decline in the housing market. Now maybe he exaggerated that a bit or not, but the data seem consistent so far.

That the economy is slowing down seems pretty obvious. This is one of the leading indicators and it is where you’ll likely see some of the initial signs of a recession. Are we in one now? No. Will one start very soon? No. Will the economy likely slow and possibly go into a recession within the next year or so? I think that is becoming more likely as more data has come available.

The problem with your “correction” hypothesis is that people may not see it simply as a merely a correction, but as signs of something more ominous on the horizon and react to that prediction. Alternatively it is also quite possible that things are bleak in terms of the economy. And finally we have your explanation. So…I see little reason to heap all of my beliefs on your view when it is only one out of at least three possibilities. Could things stabilize and keep right on going fine? Sure, but I’m pessimistic about that right now. That the Fed kept interest rates at their current value is good news…but maybe it isn’t enough.

Cheap indeed…forgive me I should have said “unshielded MRI” which means the data isn’t reliable and the economy is really…what…good? Bad? Whatever you want it to be?