Retirement Savings: Stick it in a Mattress?

Two people who know more about finances than I ever will offer retirement savings advice that I’ll not be following.

Two people who know more about finances than I ever will offer retirement savings advice that I’ll not be following.

Reuters blogger Felix Samon says (“Why people invest in stocks“) avoid the stock market like a plague.

For one thing, you have no good reason to expect an equity premium going forwards, and if there isn’t an equity premium, then your allocation to stocks should be tiny: you’re not being compensated for the extra risk you’re taking. On top of that is the question of volatility, which is not exactly the same as risk, but which again should be compensated for with higher returns, and isn’t.

My feeling is that people like to invest in stocks because they like knowing that there’s a chance that the stock market will solve all their financial problems when it rises. Think of it as a three-pronged strategy: buy a house, invest in stocks, and work hard. Any one of these three things can pay off with lots of money at retirement, in the way that investing in TIPS won’t.

What’s more, an entire generation of Americans started working and saving and buying a house in the early 1970s — and millions of them hit the trifecta, becoming successful in their careers even as their stocks rose and the value of their real-estate soared. I doubt that particular combination is going to happen again in the U.S., but the experience of that generation is so powerful as to give a lot of people a lot of hope. Even if that hope isn’t particularly rational.

The Atlantic‘s business and economics editor, Megan McArdle (“How to Save for Retirement in One Easy Step“) agrees.

If you’re saving a little bit in the expectation that your 401(k) will boom, your house will appreciate, and Social Security will support you, you may well end up in big trouble. Modern retirement planning should probably focus more on putting away an unreasonably large chunk of your income.

Granted that there’s no guarantee that stocks and housing prices will go up or that Social Security will still be there decades from now, those all strike me as a far safer bets than thinking I’ll be able to sock money away at a rate that will survive inflation.

If I were planning to retire in 10 or 15 years then, yes, I’d move a lot of my assets into low risk, high liquidity holdings. But, then, I’d have done that before the recent crash of housing and stock prices.

I’ve got another twenty-plus years, though, until I reach retirement age and, if my health holds up, I’ll probably work in some capacity well beyond that. So I’m expecting continued earnings to supplement my retirement strategy. But there’s no surefire way to make sure you don’t outlive your money.

So what would that be; a money market account or a CD paying nearly zero interest? There you’d have relatively low risk but poor (or zero) inflation protection. Stocks are better for inflation protection but they’re still not all that great. Real estate is good for both if you’re lucky and it’s liquid when you need to sell. Treasurys, maybe, if inflation isn’t too bad but still not a great return.

Essentially, today, your choices are no risk and no return or a decent return and high(er) risk. Pretty much the way its always been.

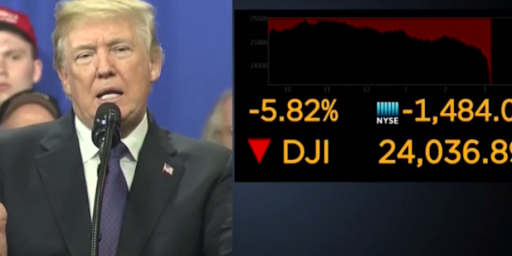

This is an exciting day to bring this up, when a (contested) rumor of Greece fleeing the EU is roiling markets.

There are a constellation of factors in this interesting topic, but to hit just a few …

That’s not what equity foes usually suggest. I think they would have you buy Treasury bonds with a maturity matching your retirement target. That is, a kid would buy 30 year Treasuries, progressing to shorter terms over time.

In retrospect, for someone in my cohort, steadily investing in a SP500 index fund, and a tax free bond fund, in the classic “your age in bonds” ratio, would have been a fair bet. It could still be.

I think Salmon is speaking to folks who are way over “may age in stocks” and don’t understand the historic risks in that, especially at high valuations (by things like PE10).

Traditional retirement advice would have you shifted largely to (laddered) bonds by that point, and with a cash-cushion for downturns.

It’s the psychology of the market and right now everybody’s crazy. Barry Ritholtz just did a compare and contrast of articles from today and 2007 to highlight the psychology. Today, 1987 crash is imminent, 2007 right before the crash, not so much.

I couldn’t really understand Megan’s “putting away an unreasonable chunk of your income”. Put it where? Not stocks or land apparently. Cash in the bank is a keystroke away from confiscation. I was under the impression that holding pieces of paper guaranteed by bankrupt governments could get real dicey real quick.

Should we invest in guns and ammo? They are the only asset that can defend themselves and other assets from being taken. They do pretty good in appreciation as well. Sure they could be banned with attempted confiscation but that just raises their value on the secondary market.

I do understand her comment if she is arguing that depending on large stock/real estate appreciation is a foolish retirement plan. Stocks may boom if we sort out the fools in DC but real estate is going to languish except for those who buy transition land that is primed to be bought for more productive use.

Although I will predict the market is going to react badly if there isn’t real change effected in the November elections. It appears the market has lost faith in the current crop of corrupt officials ability or willingness to confront the coming debt crisis.

JKB, the only true disaster insurance is physical gold, which is why that metal has become scarce in the last year or two.

(Krugerrands may sell close to the electronic spot price, but good luck finding them.)

If you are like me though, and have confidence in global capitalism in the long run, just market skepticism in the short term, there are a variety of instruments available. Sitting on some of that cash “a keystroke away from confiscation” may not earn you much, but might avoid greater peril.

This is a lousy idea. You are going to live in retirement for 20 or 30 years, if not longer. The erosion of your wealth by inflation and Heaven knows what new taxes will make you a pauper before you expect if you are trying to live off 2% CDs until your eventual demise.

Moving your money into lower risk investments is not in and of itself a bad idea, but one year of inflation can wipe out ten years of your gains in nothing flat, not to mention decreasing the value of all your holdings.

James, you’re wrong. Get a federal govt job with seniority and you might survive just about anything.

Certainly, there are no guarantees. My dad lived only to 67 and his dad before him only to 62 or so.

But the problem with holding a large chunk of your wealth in stocks near retirement — or in retirement — is that a run can wipe you out whereas inflation is a slower leak, generally speaking. So, as one gets closer to retirement, one naturally diversifies into less aggressive instruments, accepting lower gains for lower risk.

But, no, even at, say, age 60, I wouldn’t just have it all sitting in a savings account. As john says:

I consider bonds relatively low risk, high liquidity. But, at age 44, I own no bonds at all, keeping all my long-term investments in the market. Yes, I’ve taken a bath on paper. But, no, I haven’t taken any of it out.

There is a thing called bond duration. It’s important to asset allocation and flexibility (rather than literal liquidity).

We all pays our money and takes our chances.

“It appears the market has lost faith in the current crop of corrupt officials ability or willingness to confront the coming debt crisis.”

Sorry, but this is incorrect. If anything, it is the opposite. True, the PIIGS debt crisis has lingered over the market for quite awhile, but the prime instigator to this latest correction was uncertainty that Greece was going to get bailed out. Then when the EC unveiled its $1 trillion bail out plan, the market thought it might be too small–not too big. Currently, the market is worried that the austerity measures mandated by the rescue package could stymie any economic turnaround. So again, the market is worried there’s not enough spending, not too much. The market hates uncertainty, but it loves spending, at least in the short to mid term, it’s good for business. Look at what’s happened since the market lows last year, at a time when the US deficit has been exploding.

Heh

Just one comment. Beware the traditional advice.

We pays our money and takes our chances.

But there are more than a few who went all-equities 10 years ago, and now, having had a zero-return decade, feel they “need” to go all-equities again.

There are things worse than traditional advice.