Fewer Americans Are Without Health Insurance

The number of uninsured Americans has declined since the Obamacare mandate went into effect.

The number of uninsured Americans has declined since the Obamacare mandate went into effect according to three newly released surveys. The details are a bit vague.

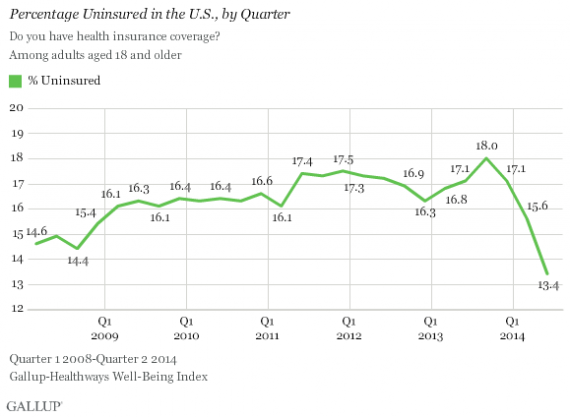

According to Gallup (“In U.S., Uninsured Rate Sinks to 13.4% in Second Quarter“) “The uninsured rate in the U.S. fell 2.2 percentage points to 13.4% in the second quarter of 2014. This is the lowest quarterly average recorded since Gallup and Healthways began tracking the percentage of uninsured Americans in 2008. The previous low point was 14.4% in the third quarter of 2008.”

The uninsured rate has decreased sharply since the Affordable Care Act’s requirement for most Americans to have health insurance went into effect at the beginning of 2014. In fact, the uninsured rate has dropped by 3.7 points since the fourth quarter of 2013, when it averaged 17.1%.

The decline in the uninsured rate last quarter took place at the start of the quarter. The drop reflected a surge of health plan enrollees in early April, prior to the April 15 extended enrollment deadline for people who had previously experienced technical difficulties with the federal healthcare exchange website. In April and May, the uninsured rate hovered at 13.4%, and it remained at that level in June — clearly indicating that the decline seen since late 2013 has leveled off.

[…,]

While 18- to 64-year-olds are most likely to have health insurance through a current or former employer (43.5%), more reported having self-funded insurance coverage in the second quarter than did before the healthcare exchanges opened in October 2013. For Americans younger than 65, 20.7% say they have a health insurance plan they or a family member pays for, compared with 16.7% in August-September 2013.

There has also been a slight increase in the percentage who have Medicaid insurance, perhaps because a provision of the 2010 healthcare law expanded the qualifying income levels for Medicaid. Thus, the reduction in the percentage of uninsured Americans has been accompanied by increases in the percentages who now have Medicaid or self-funded insurance, through a government exchange or on their own.

Now, granted, 2008 is not only too recent to provide much historical perspective it also happens to be right as the global economic crisis was kicking into high gear. And the current “lowest ever” number actually isn’t radically below the starting number. Still, presumably, most of the 2.2 point change in the second quarter can be attributed to the new law. The only caveat, in terms of this survey, is that there’s the possibility of instrument effects:

Gallup and Healthways began asking about insurance types using the current question wording in August 2013.

We have a second survey from the Commonwealth Fund showing a similar trend, however. McClatchyDC (“Survey: 9.5 million people gained health coverage in first marketplace enrollment period“):

Some 9.5 million Americans gained health coverage during the recent marketplace enrollment period as the uninsured rate for working-age adults fell from 20 percent to 15 percent, according to a new national survey by the Commonwealth Fund.

Young adults ages 19-34, whose participation in the Affordable Care Act’s coverage initiative was crucial but always uncertain, saw some of the largest coverage gains. Their uninsured rate fell from 28 percent to 18 percent.

Uninsured rates for Latinos fell from 36 percent to 23 percent, the survey found. And low-income adults earning less than 138 percent of the federal poverty level saw their uninsured rate drop from 35 percent to 24 percent.

The findings suggest the health law is meeting its goal of increasing coverage for hard-to-reach groups. Sixty-three percent of adults with new coverage through Medicaid or the insurance marketplaces were previously uninsured, the survey found.

“Adults who are being helped the most are those who historically have had the greatest difficulty affording health insurance and getting the care they need,” said Sara Collins, the lead survey researcher and Vice President for Health Care Coverage and Access at the Commonwealth Fund.

The national survey of more than 4,400 people found that in states that expanded eligibility for Medicaid, the uninsured rate among people below the federal poverty line fell from 28 percent to 17 percent. In non-expansion states, the uninsured rate for these adults fell only slightly, from 38 percent to 36 percent.

So, while the numbers are quite a bit different than the Gallup findings, the trends are robust and in the same direction. More importantly, we’re seeing what ObamaCare advocates would expect: significant increase in coverage for the targeted groups in expanded eligibility states and very little increase in others.

Finally, a new survey from the Urban Institute (“Number of Uninsured Adults Continues to Fall under the ACA: Down by 8.0 Million in June 2014“)

shows the uninsurance rate for nonelderly adults (age 18-64) was 13.9 percent (95% CI [12.3, 15.4]) for the nation in June, a drop of 4.0 percentage points (95% CI [2.6, 5.5]) since September 2013, the month before the ACA’s initial open enrollment period began. This represents a drop of 22.3 percent in the uninsurance rate, which translates to a net gain in coverage for about 8.0 million adults (95% CI [5.1 million, 10.8 million]), extending the coverage gain of 5.4 million (95% CI [3.2 million, 7.6 million]) that was found as of early March 2014.1 Though estimates of the size of the net gain in coverage vary across surveys, there is consistent evidence of ongoing gains in insurance coverage under the ACA.2

Looking across the states, we find that the states that implemented the ACA’s Medicaid expansion continued to see larger declines in their uninsurance rates for adults than did the nonexpansion states. The uninsurance rate for nonelderly adults dropped 6.1 percentage points (95% CI [4.9, 7.2]) in the expansion states, compared with 1.7 percentage points (95% CI [0.3, 3.0]) in the nonexpansion states. This represents a decline in the uninsurance rate of 37.7 percent in the expansion states and only 9.0 percent in the nonexpansion states. In June 2014, the uninsurance rate in the 25 nonexpansion states was 18.3 percent (95% CI [17.0, 19.6]), well above the 10.1 percent (95% CI [9.1, 11.2]) rate in the expansion states. Consistent with this change, the remaining uninsured are increasingly concentrated in the nonexpansion states (Kenney et al., forthcoming 2014).

Again, the numbers themselves vary from the other polls but the movement is in the same direction and differentiated among the groups in the way we’d expect. Given the size of the differences and the fact that they’re consistent across three independent surveys would indicate it’s not a polling artifact.

Interestingly, while the Urban Institute is ostensibly the most biased—it’s a progressive advocacy group, not an independent polling firm—it gives the most context for its data:

There are, however, limitations to this analysis. The HRMS was designed to provide early feedback on ACA implementation to complement the more robust assessments that will be possible when federal surveys begin releasing their estimates later in 2014 (Long et al. 2014). Though HRMS estimates capture the changes in insurance coverage from the first open enrollment period under the ACA, the estimates understate the full effects of the Affordable Care Act because the estimates do not reflect the effects of some important ACA provisions (such as the ability to keep dependents on health plans until age 26 and early state Medicaid expansions) that were implemented before 2013. In addition, these change estimates might not reflect only the effects of the ACA, because they do not control for long-term trends in health insurance coverage that predate the ACA or control for changes in the business cycle. Further, the difference in coverage gains between the states that did and did not expand Medicaid should not be entirely attributed to the ACA; there were other policy choices that likely affected enrollment. For example, many of the nonexpansion states did not set up their own Marketplaces and therefore did not get the same access to outreach and enrollment assistance funding.

All of that’s worth keeping in mind. The bottom line, though, is that Obamacare seems to be having the desired effect—both decreasing the percentage of Americans without healthcare coverage and increasing those with it.

What’s not clear from these surveys is how much of the change reflects young adults that are now covered on their parents’ plans because of the raised age limit, how much reflects those on the public dole via Medicaid expansion, and how much is a function of people previously ineligible for affordable group rates now covered under the exchanges. From an affordability and sustainability standpoint, that’s worth knowing.

The other thing not covered here is the issue of premium increases. Reports are starting to trickle out about the premium schedule that will be released for the new open enrollment period that starts 10/1, and it’s not looking very pretty.

And the Congressional Budget Office again revised down its cost estimates for Medicare, which now spends $50 billion a year less than it was projected to before Obamacare passed.

And the New England Journal of Medicine estimates that 20 million Americans gained insurance under the new law.

Basically all the end of civilization predictions by Republucans have been proven wrong.

So of course…Boehner has decided he will waste millions of taxpayer dollars to sue Obama for not properly enforcing Obamacare.

How any intelligent human being can vote Republican today is beyond me.

@Doug Mataconis:

Oh there’s that ODS…we haven’t heard from you on the ACA since the computers starting working months ago.

wow, all that money/drama for a 1% decrease since 2008- that’s just awesome!

I say again, Health Insurance does not equal “Health Care”. You need only look at the VA to see how well the majority of those with insurance gained under Obamacare will be treated.

@Doug Mataconis: And what is your particular expertise in judging premium increases and subsidization effects of premium increases?

Right now, most plans are coming in the 0% to 10% premium increase zone which is well within historical norms. There are a few outlier plans in both directions (a plan in Mississipip is looking for a 20% rate cut, Care First in Maryland is proposing 23-30% increases while Kaiser for the same market is looking at rate cuts)

throw in the fact that the Federal government is the entity on the hook for rate increases of the benchmark Silver above the rate of the change for the FPL cut-offs, premium shock won’t be visible to people shopping on the Exchange.

But that is all unpossible as there is no way a government program could be structurally well run….

@bill: Was there something that happened in 2008 that may have had systemic shocks to the US economy… nahhh… can’t be

You have to understand that in Doug’s libertarian fantasyland, there’s no way that the ACA can actually work so it’s going to be denial all the way. He takes his views on the ACA from Peter Suderman over at Reason.org who predicted that no one would sign up for the ACA and was wrong by 15 million or so. Suderman has not reconsidered, though, but still predicting unconditional disaster, much like earlier prophets who predicted the demise of Social Security and Medicare. Remember when Hayek predicted that the UK would descend into “serfdom” when the UK adopted the National Health Service? Suderman is a worthy successor to that tradition.

@Doug Mataconis:

I’d like to see more about this…the only thing I’ve been able to find is a vague guess from Wellpoint back in March about double-digit increases…which every analyst found surprising and assumed was just Wellpoint being conservative and covering their arses.

Also in March Wellpoint, a private sector company, raised it’s earnings forecast from $8 a share to $8.50 a share based on the 1 to 1.3 million new customers that our Socialist Tyrannical President sent them.

@Jack: But those people are getting private insurance from insurance companies or Medicaid. Why would their care be different at the doctors or at hospitals. There’s no big red “O” sticker on their insurance cards.

A study from the Commonwealth Fund shows the majority of people insured by Obamacare are very happy with it.

http://www.vox.com/2014/7/10/5887105/for-millions-who-signed-up-obamacare-is-working

The saddest thing about this is that the majority of Republican governors are actively lying to their citizens to keep them from benefiting from this program. Whether it be Obamacare or children on the border, the Republicans would rather see people suffer than allow Obama to get credit or even avert disaster. They have no solutions of their own.

@beth: It’s not about a big “O” on their insurance card, it’s about insurance companies limiting the number of provider available in network for those with Obamacare insurance. The end result is plans that employ a version of rationing — either by distance or long wait times to get an appointment.

Additionally, while the ACA has thus far added 7-9 million people to the system, it does nothing to add doctors. Between Obamacare, Medicare and Medicaid bludgeoning doctors to accept less and less for their services, older doctors are closing up shop and those who remain are shortening their time with those patients they do see. It forces doctors to race through medical appointments so they can fit as many into the daily schedule as possible.

Without a doubt, the consequences are being passed on to patients.

@Jack: So it’s better to not have insurance than to wait to see a doctor? Okay then.

@Jack:

ALL plans, private or public, government-run or not, employ a version of rationing, whether by distance, wait time, price, or a combination thereof.

You know why? Because EVERYTHING that’s not unlimited is rationed one way or another. The supply of Porsches and Ferraris is rationed by price, for god’s sake.

@beth: Well of course, if we’re talking about other people….

@Jack:

Source please.

Health care is a market place. With more customers having a great ability to pay, and greater demand, hiring of doctors and nurses will increase. There is almost always a lag between an initial demand and a market’s response.

Source, please.

Source, please.

@Jack:

How would having those people go without insurance add doctors to the system?

Newsflash! Thing not designed to do something does not do the thing it is not designed to do!

@Doug Mataconis:

…. and this is different form the status quo in what way exactly ? You never really had to wade into the non-group insurance market have you 🙂

@Jack: Evidence for a flood of early retirements as I work in the insurance industry and there is nothing that I’m seeing about unusual exits

@Doug Mataconis: @Doug Mataconis:

…. and this is different form the status quo in what way exactly ? You never really had to wade into the non-group insurance market have you 🙂

@Neil Hudelson:

Conservatives believe in the market — except when they don’t. They should almost come with one of those advisories you get on some TV commercials, like “warning: core beliefs may not apply when not convenient or when president is a Democrat.”

@Jack: RomneyCare was signed into law eight years ago. Did any of the bad things you mention happen in Massachusetts? Hawaii expanded its medical insurance coverage a long time ago using a different mechanism. Did any of the bad things you mention happen in Hawaii? If you want to be believed, provide your sources.

@beth: Someone who has private insurance has access to many more doctors than those on Obamacare, medicare, or medicaid. Period. Having health insurance does not equal healthcare. Waiting for a procedure could mean the difference between life or death. Additionally, having to drive an hour away to find an in network provider or having to pay out of pocket to see someoone local during an emergency is not a good trade off.

Even hospitals are refusing Obamacare patients.

http://health.usnews.com/health-news/hospital-of-tomorrow/articles/2013/10/30/top-hospitals-opt-out-of-obamacare

@Jack: And again I ask you how the people without insurance before Obamacare are worse off now? It’s not a question of having less providers to choose from – before they had insurance they had no providers except the ER to choose from. How are they worse off now?

@Jack:

Like if you have no health insurance and have to wait forever because you can’t pay?

@beth:

Less freedom.

@Neil Hudelson:

http://www.washingtonpost.com/national/health-science/insurers-restricting-choice-of-doctors-and-hospitals-to-keep-costs-down/2013/11/20/98c84e20-4bb4-11e3-ac54-aa84301ced81_story.html

http://www.forbes.com/sites/brucejapsen/2014/01/29/doctor-wait-times-rise-as-obamacare-rolls-out/

http://www.theihcc.com/en/communities/policy_legislation/the-new-health-law-bad-for-doctors-awful-for-patie_gn17y01k.html

Google is your friend, you should try it.

@Jack: Not all private insurance plans for group sponsored coverage is broad network. My company’s three biggest selling plans are restricted network plans. The biggest selling plan since 2003 includes 35% of the total hospitals and 80% of the individual docs of the broadest network. Companies buy this plan becuase it is 25% cheaper than the broad network. Please note the date when this narrow network product was offered.

@Rafer Janders: Freedom to go bankrupt, freedom to go to the corner and die quietly. Your concept of freedom is a rich man’s freedom.

Your figures, James, make the assumption that these folks have paid into the system

and, there’s still the question of, assuming they HAVE paid, that they can actually GET healthcare, given the problems of doctors who wont touch the system, and the huge deductables.

@Rafer Janders:

The ACA mandated free visits for preventative/checkups. Adding 7-9 million people that in the past would only see a doctor when they were sick that are now trying to seei doctors every 6 months for preventative care by definition, increases the number of people seeing doctors without actually adding any doctors.

@beth: Because at least they could be seen in the ER. Now, their local ER is likely not even in their network so they will either have to pay out of pocket or not pay at all for the ER services, thus, we are no better off than we were before when it comes to taxpayers having to foot the bill.

@Stan: I’m not “projecting” bad things, I’m linking to “actual” bad things.

Let’s break out some of the new data, shall we:

But wait, what? Did I just see that? Let’s pull out one very special sentence:

Oh, and there’s more.

So, Republicans who actually experience Obamacare love it, and no, there are no long waits.

That would make the Obamacare haters wrong on every single scare they’ve ginned up. Wrong, wrong and wrong.

@Rafer Janders:

How does Obamacare, Medicaire, and Medicaid increase the number of customers who “can” pay?

Greater demand??? Paying less for a product than it’s cost does not increase the number of people willing to produce that product.

@Jack:

So you claim that doctors are deliberately curtailing their time with patients, I ask for a source, and you link to an article that says doctors offices are increasing use of medical care providers like Nurse Practioners, makes no mention of doctors deliberately curtailing their time, and is essentially an article about how people with health insurance are visiting doctors. Great job backing up your argument.

Then you follow it up with a link that predicts longer wait times, but provides no evidence that its happening.

Google, apparently, is not your friend.*

*I really don’t know why multiple commentators think its the duty of the audience to research their claims, rather than provide evidence on their own.

@Jack:

…really? People had no insurance could not visit a doctor. Now they have insurance–i.e. a vehicle to pay for health care.

Again, you need to provide evidence that, as a whole, Obamacare is resulting in payment for health care that is less than the cost of health care. No, finding one subset does not count, as this is a discussion of Obamacare as a whole. An no, I won’t google it for you.

Second, what do you not understand about demand? More customers are entering the marketplace with an ability to pay for health care.

@Jack:But if they’re still going to the ER even if they’re not covered in their network (they weren’t covered by anything in previous ER visits) we’re no worse off either by your logic.

You don’t know a lot of people without insurance, do you? I do. People who have treatable diseases such as diabetes, high blood pressure, migraines, etc who could never see a doctor before they had insurance. They’re not going to the ER and they’re very happy to take whatever doctor care is being offered in their plans. And I don’t know anyone outside of infancy who goes to the doctor every six months for preventative/well care.

@Jack:

Jack, explain something to me: why do 74% of newly-insured Republicans like their nice new Obamacare policies?

Those are Republicans who have actual, personal experience with actual facts, as opposed to talk radio brainwashing. Explain, please.

@michael reynolds: Yeah, looks like these people are really satisfied with their Obamacare.

http://sanfrancisco.cbslocal.com/2014/04/18/consumerwatch-some-covered-california-patients-say-they-cant-see-a-doctor/

http://www.huffingtonpost.com/2014/04/10/obamacare-patients-without-doctors_n_5044270.html

http://www.dailykos.com/story/2014/04/25/1294762/-Doctor-Refuses-Patient-Because-She-Has-Obamacare

http://www.kvoa.com/news/tucson-doctor-refuses-to-see-obamacare-patients/

http://money.cnn.com/2014/03/19/news/economy/obamacare-doctors/

@Jack: Obamacare reimbursement rates range from Medicare plus a bit to full commercial rates — it depends on the company, the plan and the network.

please get a clue.

@Neil Hudelson: From the very article I linked…maybe if you actually read the links, you would find the information I provided.

Medicare reimburses hospitals and doctors, on average, 71 and 81 percent, respectively, of private rates.7 Medicaid reimburses doctors even less, on average 56 percent of private rates.8 The federal government’s payments to health care professionals are so low that on average, overall, hospitals lose money caring for Medicare and Medicaid patients. In 2008, hospitals received only 91 cents from the government for every dollar spent on a Medicare patient. That same year hospitals received only 89 cents for every dollar spent on Medicaid patients.

http://www.theihcc.com/en/communities/policy_legislation/the-new-health-law-bad-for-doctors-awful-for-patie_gn17y01k.html

Most of the customers entering the market do not have an ability to pay. They are medicaire patients or they are getting subsidies.

@michael reynolds: From your article:

“It may also be a sign that those newly insured people are relatively sick and will be particularly expensive to insure. Commonwealth found that about 70 percent of people using their plans had a pre-existing health problem.”

Regardless of the political stripe, if 70% have pre-existing conditions, of course they are going to like their nice new Obamacare policies.

@beth:

Yes, we are worse off. We are already paying for their medical coverage through Obaamcare, yet if they go to an ER that is not part of their network and cannot pay, that money must also be recovered–from taxpayers.

@Jack:

I read that part and saw no indication that 71% and 81% of private rates equates to below cost of production. Additionally, the main thrust of Obamacare was placing people on privately funded insurance plans, not medicare. So, again, please show me how people on insurance because of Obamacare, because either you are being deliberately obtuse or you do not understand the fundamental thrust of Obamacare.

75% of enrollees are under the age that medicare would be an option. The others–even if they do receive subsidies–are enrolling into the private marketplace. So, again, your above figures don’t apply to 3/4ths of the enrollees, and for the other 1/4th, there isn’t evidence to back up what you are claiming.

http://www.cnn.com/interactive/2013/09/health/map-obamacare/

You aren’t very good at this.

@Jack:

Jack, on your side you’ve got a random collection of anecdotes. On my side I have a professionally conducted poll. Which do you think is the better data?

Of course you’ll say it’s the random collection of anecdotes, because hating Obamacare is an article of religious faith for you guys. But dude: it’s over. We won. You and Fox and Sarah Palin and Rush Limbaugh have nothing. Zip. You’re done.

Jack, I think you have a misconception about Obamacare. It is not a health insurance policy on its own but rather a system that allows matching consumers with private insurers. That’s why they needed the complicated web enrollment process. As such, patients don’t have a card marked “Obamacare”, they have a card marked “Cigna” or “BlueCross/Blue Shield”. Providers don’t know they are Obamacare patients.

When I was shopping for insurance late last year the difference between what Obamacare offered for Kaiser and what I eventually bought directly from Kaiser was essentially nothing.

Once in a while there is a discussion about something I happen to know about, usually because of my job. The changing environment for health care is one of those things. And there is a lot of ignorance being shown here. For instance:

– Almost all plans have limitations on which doctors are in network or which are out of network. This is not new, nor does it have anything to do with Obamacare.

– There has been a steady trend for decades of fewer and fewer physicians becoming family physicians. The trend has been to specialize.

– Warning: Personal anecdote – When I lived in the Northeast and had a very, very good health plan, we needed to schedule appointments for surgery, procedures, etc. And sometimes the wait was weeks or even months. This seemed to be the norm and has been true no matter where I lived in the US.

– There has been a trend for a number of years for hospital groups to buy up more hospitals and now to buy up family physician groups. Some doctors hate it but I know many who are happy to have a salary and not worry about insurance claims or have to be on call 24/7

– And the idea that hospitals are avoiding Medicare/Medicaid patients in any significant volume is completely and totally absurd. I can’t even begin to describe how absurd this is. Suffice it to say that despite paying less than the average for private insurers, the total dollar volume of hospital business for M/M is now just over 50%. There isn’t a major hospital in the country that could walk away from 50% of their revenue. They would have to close their doors tomorrow. In some Florida and Arizona hospitals it is closer to 70%.

@Jack: “Medicare reimburses hospitals and doctors, on average, 71 and 81 percent, respectively, of private rates.”

Which is exactly how insurance companies operate. For my recent hospital stay, they billed a $48,000. (For three nights. Not including… well, most everything.) The insurance company said “we’ll give you $21,000. The hospital accepted that.

I’m not a math genius, but it seems to me that my insurance company was reimbursing at a lot lower rate than 81 or even 71 percent.

@MarkedMan:

Shhhh, those are just facts buttressed by expertise. Such things have no part in the Obamacare debate.

If you want any credibility with Jack and his fellow travelers you’re going to have to explain how the death panels are killing off white folks.

@Jack: “Regardless of the political stripe, if 70% have pre-existing conditions, of course they are going to like their nice new Obamacare policies.”

Well, yes. Because under the old system they would be unable to get insurance. That’s the point, it’s not a bug.

@wr:

Yes, funny how that works. People who couldn’t get insurance like getting insurance which was pretty much the point of Obamacare.

For Jack, if he comes back:

Even 77 percent of people who had insurance before — including members of the much-publicized group whose plans got canceled last year — were happy with their new coverage.

There is no good way (IMHO) to discuss the financial aspects of hospital care vis insurance companies. The hospitals put a price tag on a given procedure which they completely ignore in negotiating with insurers in confidential agreements. The result is that the ‘official’ price put on a procedure can differ by amazing amounts at two hospitals within blocks of each other. Medicare/medicaid apply what limited stability and sanity to this set up. In addition hospitals are wonderful at finding ways to get checks from state and local governments that do not apply to individual patients but ‘reimburse’ them for indigent care, for example.

The bottom line is that the last party to be pitied in this extremely complex stew is the nation’s major hospitals. Small local not-for-profit hospitals in non-medicaid-expansion states, they desperately need help. Big medical centers are doing well enough to buy art and give $million bonuses.

@Jack: Which is so much worse than not being able to get health insurance because of “prior conditions”, or discovering that when you’re half-way through your cancer treatment your health insurance provider has decided to yank your coverage because you didn’t tell them about an asthma medication you took when you were a kid?

I grumped about Japanese National Health Care service when I was in Japan, but after dealing with the US health care system I’d exchange what we have here for it in an eyeblink.

(How many people posting here about how EEEVIL Obamacare is have experienced living under any other country’s health care system?)

@Jack: Emergency Rooms are covered by all health plans. They’ll hit the user up for a high co-pay/deductible but an emergeny room down the street from me and an emergency room three time zones over from my office will be treated as if they are both in-network until I am stabilized. At that point, out of network charges come into play.

@Jack:

Um…Obamacare is private insurance.

Keep the Government out of Medicare, right Jack?

@Eric Florack:

Myths…every single one a right-wing myth.

I think, for all the railing and research Jack has done, he actually doesn’t understand how Obamacare fundamentally works. It’s almost like someone googled “How is Obamacare bad” and just went from there.

@Neil Hudelson:

Yeah. . . almost like that.

@ Jack

You do understand that regular check-ups and preventative care vastly reduce overall stress on the system by catching problems earlier and keeping people more healthy in general.

Don’t you?

@Richard Mayhew:

Um, that was sarcasm, Richard.

@Jack:

Ah, so your solution to the problem of “there aren’t enough doctors for everyone” is “7-9 million people should just go without doctors.”

Genius! I mean, of course — instead of adding medical doctors, we can just deny doctors to millions of our fellow citizens! That will free up the existing physicians’ time so they can spend more of it with their richer, better insured patients.

Not sure what those 7-9 millions who’ll have to forgo doctor visits entirely should do, but I’m sure if they do get sick, we can, uh….[insert hand wave here].

@Jack:

Obamacare IS private insurance. Obamacare isn’t like Medicare or Medicaid, rather, it matches up consumers with private insurance companies. You don’t have an “Obamacare” insurance policy, you have an insurance policy through Blue Cross, Aetna, etc. etc. that you found via the Obamacare website. The actual insurance is handled by a private, for-profit company. Period.

@Jack:

First, those 7-9 million people didn’t have medical insurance, then they often didn’t see a doctor even when they were sick.

Second, many of them had chronic medical conditions such as arthritis, depression, heart disease, diabetes, bursitis, MS, bronchitis, high blood pressure, alcoholism, anxiety, emphysema, asthma, hemophilia, HIV-AIDS, Parkinson’s disease, etc. etc., so “when they were sick” was pretty much “always.”

@Jack:

And I have it on good authority from “jim m” that many people won’t drive an hour across town to save their child who is dying of leukemia, so this makes perfect sense. An hour’s drive doesn’t seem a good trade off compared to not having any medical insurance at all.

@Jack: Exactly so.

Which means the left won’t like you much.

@anjin-san: and where do they get those? And given the far higher deductables, how do they pay for it?

@ Florack

So far, all you have produced is some yap. Cites (from credible sources) would be nice. Or have you just bough into all the right’s BS about Obamacare hook, line, and sinker?

I really wish that those ranting about Obamacare be zipped back in time and have to try to find health insurance while being out of work with a pre-existing condition. You know what? There WAS no health insurance for such people. Zip. None. If you had diabetes they wouldn’t take you. If you had a history of cancer they wouldn’t take you. If you had already hit the lifetime cap they wouldn’t take you. And if you went to a hospital to pay out of pocket you had to pay the complete, full, inflated price rather than the half or two-thirds less price the insurance companies were able to haggle down to.

And you want to go back to that?!!!

@Grumpy Realist:

Man, if you’d had a bad head cold they wouldn’t take you.

@Richard Mayhew: obama won the election, what else?

but seriously, wheres the “30+ million” that he was touting with this plan that over 60% of the populace didn’t want? and now they’re getting a chubby about a few million people who had to sign up, but may not pay when they get the bill? so again, a 1% decrease was really worth all that bs?

@ bill

Have you noticed that most Republicans who actually know anything have stopped talking about Obamacare? There is a reason for that, and it’s not “Obamacare is a joke”…

@bill: ” a few million people who had to sign up, but may not pay when they get the bill? ”

Hate to tell you this, but you’re still on February’s talking point. They did pay when they got their first bill. Oh, and the young folk are signing up in sufficient numbers, which explodes March’s talking point.

If you’re too lazy to check out Redstate for yourself, the current talking point is “Obamacare is evil because — look, Benghazi!”

@wr: Yeah, it’s funny how now that it looks like this thing is working, the talking points have switched to what’s going to happen next year (see Doug’s comment). “Well sure, it’s working now, but just you wait till 2015 and the prices go way up.” Come 2015 and the predicted disaster doesn’t appear? Well then they’ll just switch to forecasting doom and gloom for 2016. Lather, rinse, repeat.

@Jack: Given that you’ve seperated “Obamacare” from both private insurance and from Medicaid and Medicare I want to know what you think it is– I mean you do realize that the non-Medicaid/Medicare patients added by the Affordable Care Act are on private insurance right?

Not surprisingly Florack has gone dark…

@anjin-san:

He just comes for the spankings.

Imagine how many more people would be insured (or, how much fewer uninsured there would be) if Republicans implemented ACA in the states that are controlled by Republican governors and legislatures.

@Jack:

Jack, a health insurance policy purchased through an state exchange is not a government health insurance policy, it is a policy, with an array of options, similar to the choices many people have when they select from plans offered by their employer (which are provided by private insurance companies.)