The image is released free of copyrights under Creative Commons CC0.

The New York Intelligencer‘s Eric Levitz contends “The ‘Greedflation’ Debate Is Deeply Confused.” The relevant bit of the setup:

[M]ainstream economists argue that today’s inflation was born out of a mismatch between demand and supply. The pandemic recession reduced the global economy’s productive capacity by shuttering factories, disrupting supply chains, and nudging many older workers into retirement. At the same time, a series of historically large relief packages increased U.S. consumers’ purchasing power. Virus-averse consumers then shifted their copious disposable income away from in-person services and toward goods en masse. Demand for myriad manufactured products therefore soared while supply fell. This enabled producers to command higher prices for their wares. And it also encouraged them to rapidly expand production by hiring more workers, thereby pushing up the cost of labor. This, in turn, increased costs for providers of services like childcare facilities, physical-therapy clinics, and fast-food restaurants. A general and persistent increase in prices ensued.

Some progressives suggest that this account is all wrong: Today’s inflation has little to do with fiscal policy or demand conditions. Rather, it is the product of a frenzy of profiteering in the corporate sector. In my view, their case is weak.

More precisely: There is a crude version of the “greedflation” argument that is obviously wrong, and a sophisticated version that is plausible but unproven (and which does not actually refute the relevance of demand conditions).

That the post-COVID inflation was caused mostly by “greed” is so absurd that it’s hard to believe anyone is taking it seriously. Greed, after all, is the natural condition of the capitalist. If companies could raise prices on a whim, they’d have done so long before the pandemic.

The crude version of the greedflation argument, as articulated by former Labor secretary Robert Reich and The Lever, goes (roughly) like this: The relationship between the demand for, and supply of, goods and services has little to do with inflation. Rather, rising prices are a product of excess corporate power. As Reich writes, “Corporations have the power to raise prices without losing customers because they face so little competition.” And they face so little competition because, “since the 1980s, two-thirds of all American industries have become more concentrated.”

This raises an obvious problem: Corporate concentration has been transpiring over decades. In 2019, U.S. industries were roughly as concentrated as they were in 2022. Yet in the former year, inflation sat near 2 percent, a low level by historical standards. In the latter year, by contrast, prices rose by 6.5 percent. So why did corporate concentration yield historically low inflation throughout the 2010s, only to suddenly produce exceptionally high inflation following the pandemic?

Reich acknowledges that the pandemic did increase corporations’ costs, raising the price that manufacturers must pay for energy, metals, and workers. But companies then used these genuinely higher costs “as excuses to increase their prices even higher” than necessary for offsetting those costs. Empowered by such excuses, and sheltered from competition by market concentration, avaricious companies powered inflation through price gouging.

So, that’s certainly more plausible. But, again, profit has always been the goal. Firms were never constrained in their pricing by mere “necessity” but by what the market would bear. Absent collusion—which has been illegal for a very long time—they have to worry both about being undercut by competitors and by consumers rejecting their product for substitutes.

The idea that market consolidation that has created behemoths like Amazon allows those firms to raise prices because consumers are essentially trapped is appealing. But it’s not exactly a sudden phenomenon.

But that’s basic economics. Why are smart people like Reich falling for it?

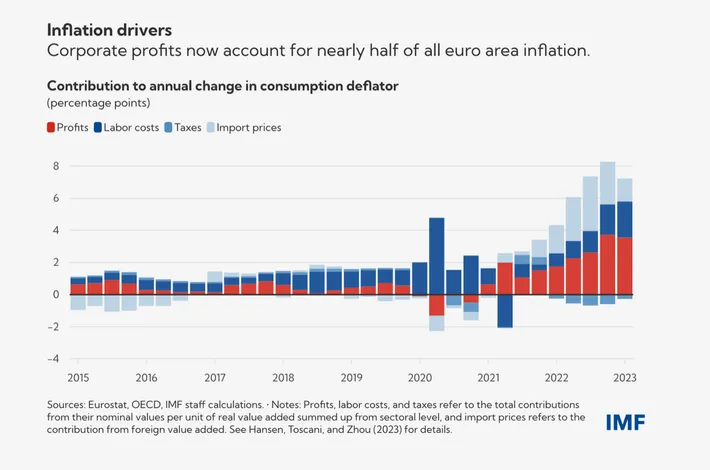

The primary evidence for this claim is the correlation between rising inflation following the pandemic and an increase in corporate profits. Between the fourth quarter of 2019 and the second quarter of 2021, pretax profit margins jumped from 15.6 to 17.9 percent. Proponents of the greedflation hypothesis will often support their argument with charts like this one from the IMF, which shows that profits “account” for far more of inflation in the euro area than labor costs do.

That’s actually pretty compelling, right? The red boxes (profits) are getting bigger and the dark blue boxes (labor costs) are going down!

But, again, if corporations could simply jack up their profits whenever they wanted, they’d do so all time time.

There are several problems with this argument.

First, it is unclear why corporations would feel compelled to wait for an “excuse” before seeking to maximize their profits. Ironically, Reich’s version of the greedflation thesis implies that corporate America put the public good above its own financial self-interest for years if not decades: During the 2010s, corporations could have charged much higher prices for their goods, as they were insulated from competition by concentration. But for years and years, they decided not to maximize their profits, since they lacked a compelling “excuse” for charging a financially optimal price.

This is an odd theory of corporate behavior. Generally speaking, companies do not feel compelled to provide an excuse for pursuing their mercenary interests. As Reich is keen to highlight in other contexts, U.S. firms have been perfectly happy to offshore jobs to low-wage areas, even in the absence of an economic crisis that would serve to rationalize such profit-maximizing endeavors. Pharmaceutical firms, meanwhile, routinely price-gouged on life-saving medicines, even when inflation was near historic lows.

A second problem with the crude version of the greedflation thesis is that the correlation between rising profits and rising prices does not actually tell us much about the cause of the latter.

Well, sure. But the fact that they’re making excess profits during a pandemic and post-pandemic recession—with President Biden getting blamed for it!—is bad, no?

Let’s stipulate that the conventional theory of post-COVID inflation is correct: Fiscal policy enabled demand for goods to outpace their supply, as the economy struggled to ramp up productive capacity following the pandemic recession. In that scenario, producers of goods would see the market value of their wares increase, since such goods would be scarce while consumer appetite for them would be abundant. This would make it possible for firms to secure a higher price for their goods, and therefore, to earn higher revenues. Those higher revenues would then either go to workers in the form of higher wages or owners in the form of higher profits, depending on the balance of power between labor and capital within the firm. But in either case, higher wages or higher profits would be an effect of the inflationary environment, not its cause.

Which makes sense, right? If car dealerships are being supplied fewer cars than customers are wanting to buy, they’re obviously not going to be very interested in negotiating lower prices for them. Indeed, they’re likely going to be able to command prices above MSRP. That is, I supposed, greedy. They could just sell them at 2020 prices. Or, only enough above 2020 prices to recap whatever additional costs they’ve incurred. But that’s never been how businesses operate.

Indeed, Levitz turns that example himself:

Matt Bruenig helpfully illustrates this point with reference to inflation in the used-car market. Following the COVID recession, demand for personal vehicles outstripped their supply. This was largely a result of a shortage in semiconductors, a key input into modern automobiles. During the pandemic, consumers suddenly increased their spending on various electronics that use semiconductors. At the same time, COVID lockdowns in China (among other things) restricted the global economy’s capacity to produce chips. As a result, carmakers lacked the inputs to crank out autos at a normal pace.

Unable to secure new vehicles, consumers turned to the used-car market. The price of used cars accordingly skyrocketed. Between June 2020 and January 2022, the price of a used car in the United States jumped by nearly 60 percent, after previously holding steady or declining for 25 years.

Sellers of used cars did not see their costs increase; such sellers have virtually no costs since they’re selling an already completed product. As a result, the increase in prices in the used-car market went almost entirely into higher profits. In the phrasing of the IMF chart above, profits would “account for” nearly 100 percent of used-car inflation.

But that wouldn’t mean that profiteering by car owners “caused” that inflation in any meaningful sense. The used-car market did not grow suddenly more concentrated after the pandemic recession, nor did car owners suddenly become more greedy. In the aggregate, they have always sought to get the best price they could for their vehicles. That “best price” simply increased due to a mismatch between the demand for, and supply of, used vehicles.

Indeed, it wasn’t just sellers of automobiles. Both the state of Virginia and the county where I live impose an annual property tax on automobiles. Our tax bill went up considerably even though the cars were all a year older because their market values went up. Ditto the property tax on our home. The fact that we didn’t sell them or realize a profit on them didn’t matter in the slightest.

Proponents of the greedflation thesis suggest that their analysis has recently been vindicated by reports from the Kansas City Federal Reserve and European Central Bank. But as Bruenig notes, these claims rely on misreadings. Both reports note that profits have contributed to inflation more than wages. But in doing so, they are merely (awkwardly) describing the distribution of inflation’s benefits, not its causes. When discussing actual causal mechanisms, the ECB suggests “demand outpacing supply in many sectors” as one critical factor. The Kansas City Fed, meanwhile, explicitly rejects “the simple explanation of ‘greedflation,’ understood as either an increase in monopoly power or firms using existing power to take advantage of high demand.”

Notably, as the economy’s productive capacity has recovered, and supply has grown less constrained, profit margins have fallen. In the first quarter of 2023, pretax profit margins were back down to pre-COVID levels, even as inflation persisted (albeit, at a decelerating pace).

So, as the economy slowly gets back to normal, so do profit margins?

The final problem with the crude greedflation argument is that it simply ignores the very strong evidence behind the conventional account of the post-COVID inflation. Congress really did mount a historically aggressive response to the pandemic recession, providing households with so much financial aid, Americans’ disposable income actually increased during the economic downturn and has remained above 2019 levels ever since.

At the same time, fear of contagion led consumers to suddenly, collectively shift their spending away from in-person services and toward goods en masse, producing an abrupt surge in demand for goods.

Combine this with battered supply chains and a shrinking labor force (as many older Americans opted to retire all at once), and we would expect to see inflation, irrespective of corporations’ greed or market power.

Which, oddly, was the story we were being told in real time.

In sum, the crude greedflation argument has no satisfying explanation for why prices rose when they did, relies overwhelmingly on a correlation that does not imply causation, ignores copious evidence that a mismatch between supply and demand has been the primary cause of inflation, and cannot account for the fact that price growth has persisted in 2023 even as corporate profit margins declined.

Yet Levitz’s article goes on considerably longer. Why? Well, because there’s a version of the “greedflation” argument for which there is at least a modicum of support: that firms all along the supply chain padded their profit margins a little bit because they could get away with it.

During periods of low inflation, price increases are conspicuous and consumers react to them. Big, flashy price increases run the risk of consumers abandoning your product and substituting something else.

But when the economy is chaotic and inflation is already high—and consumers are faced with endless news coverage of it—these constraints ease. If inflation is running at 8% and everyone is panicking, it’s barely noticeable if a bag of Cheetos goes up 8% or 17%. It just seems like yet another wild price increase, like eggs or beef or used cars experienced for a while. At the same time, there’s little risk of your prices being undercut, not because of corporate concentration but because everyone else is suffering supply shortages at the same time.

Levitz cautions that the evidence for this is decidedly mixed but it would hardly be shocking behavior.

This analysis ignores something else significant. I will agree that at least some of the inflation had external causes (supply chain interruptions, labor shortages, etc.), and it is difficult to determine what percentage of the increases were from the external causes and what percentage were from sellers padding their profit margins.

However, as the external causes of the inflation surge have been alleviated, prices remained at the higher levels, rather than competition pushing prices back to pre-COVID levels. This is hard to explain, without attributing it to greed. This is suggested by the IMF chart you cite, where the corporate profits portion of inflation increases has grown in the last few quarters, even as supply chain interruptions have lessened.

Rents increased rapidly when people were receiving pandemic money. Now that money is no longer coming in, rents are no longer increasing as much. They’re also not coming down as their tenants income decreases. I doubt landlords are the only business folks who take advantage of opportunities like this to further feather their shareholders’ nests.

The article is pretty ridiculous and admits that corporate profiteering may have led to inflation. But it would be wrong, morally, to make a morality play out of it. Morality is only for the little people, I guess, like the moral hazard of forgiving student loans.

One of the articles Levitz mentions has the chief economist from UBS saying that recent inflation has been driven by profit-seeking. This is just a weird piece about a crude strawman intended to lull people into believing what they’re told.

If companies could raise prices on a whim, they’d have done so long before the pandemic.

But, as several of the commenter you quote at least imply, the COVID-related supply shortages had the side effect of increasing the monopoly power of large providers in numerous markets. They couldn’t raise prices before because there were too many competitors who could undercut them — but under COVID those competitors were pushed out of that market (or at least reduced as a significant factor) by supply issues. That’s what changed.

…and as noted by @becca, price elasticity is not symmetric. Prices go up much more quickly than they come down, even if the economy returns to its previous state. It’s a ratchet — it sticks at the current level, and can really only move in one direction barring major recession. Any opportunity to raise prices temporarily becomes permanent.

As Reich writes, “Corporations have the power to raise prices without losing customers because they face so little competition.” And they face so little competition because, “since the 1980s, two-thirds of all American industries have become more concentrated.”

Reich has been pointing this out for decades, ever since antitrust regulators started accepting the absurd argument that consolidation will actually lower prices because of efficiency. And his premise is correct: highly concentrated industries main reason for not raising prices is concern that consumers will buy less of their products. But once prices have been raised and accepted as the new normal, they have no incentive to lower prices since they have little competitive pressure. Covid provided a reason to ratchet prices up, and there is little competition to bring it back down.

Reich’s analysis is far from faulty. It’s dead on.

I’m reminded of back in 2009, my employer made a significant reduction in what was covered by our health insurance while jacking up what we paid for it, and claimed this was a result of new Obamacare requirements. This made no sense because our employer self-insured and wasn’t even covered by the law.

After complaining about this to someone I knew in HR, they confided that the company was lying because they knew half the employees would believe anything bad that happened healthcare related that was blamed on Obamacare, so it was a great way for the company to reduce the value of benefits and have most of the work force blame someone else for it.

The reason I’m bringing this up now is that I suspect the answer to the “why didn’t the corporations do this before now?” is similar. They’ve discovered that nebulous “supply chain problems” is a great excuse for all kind of things, from inflated prices to crappy service and a big chunk of the public will blame someone else for it.

Absent collusion—which has been illegal for a very long time

The problem is that like a lot of regulations, Republican judges have so watered down these laws that it’s nearly impossible to enforce these laws unless a particular company is dumb enough to more or less publicly confess to it.

For example: right now 90% of the commercial landlords in the US use the “asset optimization algorithm” from the same company, RealPage, to “recommend” the rental amounts for their properties. Now by any reasonable definition this should be considered a price-fixing cartel, but since everyone involved claims that’s not their actual motivation, it’s more or less impossible to prosecute.

@Modulo Myself: Hey now! If we start forgiving student loans, how are we going to keep up the number of poor people desperate for work at even low wages that we’ll need to keep wages depressed? It all works together. It’s not two different models and never has been. It’s all factors in one system.

They’ve discovered that nebulous “supply chain problems” is a great excuse for all kind of things,

I’m reminded of the DISH TV commercial, where the child is selling 6 ounces of lemonade at a sidewalk stand for 5 dollars, and explains that the cost is due to “supply chain problems”.

Or recently my church reported a 50% increase in income from selling perogies (as compared over the past ten years). They didn’t sell any more volume (in fact the volume fell) what they did was increase the price (blaming ingredient increases during the pandemic), to maintain their pre-pandemic margin. Since those costs decreased beginning late summer, they kept the same pricing but effectively saw a 300% increase in their margin.

IMO, what would be revealing in the discussion of inflation is some data on margin.

Can the corporation selling widgets with a 20% margin, justify increasing that margin to 80%?

OTOH, in a capitalistic environment, accumulating evermore wealth is the objective, regardless.

Let me paraphrase: That greed caused inflation is absurd but greed is the natural state of capitalism. Amazingly, these two separate and contradictory thoughts are next to each other. So despite the above, let’s just say that inflation is not clearly understood by economists but it probably has many causes, and yes, greed probably is a contributing factor. Historically, oil prices have been the main driver for inflation, but as stated, many other reasons exist such as surplus capital, tight supply chains, and scarcity. The bottom line is that each element can contribute to inflation and it is usually a combination of factors.

That’s actually pretty compelling, right? The red boxes (profits) are getting bigger and the dark blue boxes (labor costs) are going down!

Yup. This graph shows the story.

I think all that’s left is to argue about what happened during that time period that let corporations increase prices without getting hit by consumers fleeing to competitors or cutting back.

If you don’t like ascribing emotional reasons to companies, you could reframe the corporate greed as price resistant markets or something.

But once prices have been raised and accepted as the new normal, they have no incentive to lower prices since they have little competitive pressure. Covid provided a reason to ratchet prices up, and there is little competition to bring it back down.

Except that inflation has always had a ratchet effect, including prior to the consolidation, Reich talks about.

And if his theory had any merit, we’d see the highest inflation in the industries that have had the most consolidation since the 1980’s – is that what we actually see? Here’s one chart and I don’t see any obvious pattern that would suggest that Reich is correct.

Also, we have constant inflation except when we’re in a recession or depression. Prices increasing by the Fed’s target rate of 2% a year for three years vs 6% for one year are both going to ratchet. Inflation in the 1970’s – before Reich’s consolidation, ratcheted.

So I think Reich is wrong – what we’ve seen over the last couple of years is almost entirely about supply and demand creating inflation, not a few greedy industries creating it.

We had a situation where demand for some things plummeted while it spiked for other things. At the same time, supply was constrained. That is always going to cause prices in significantly increase.

That is always going to cause prices in significantly increase.

There’s very little in the way of competition in most markets so corporations are extremely reluctant to let go of those extra profits. Look at what Nvidia did for the 40 series of graphics cards (their latest generation). They cost +$200 more than the last gen 30 series versions and provide the same or less performance. This despite TSMC’s yields resulted in a reduced silicon cost. So Nvidia not only are using chips that are cheaper than the prior generation they also cut back on the ram side to save even more money. NVidia pocketed all those savings and decided they wanted to still make hundreds more per card than they did last generation. Since Nvidia has 70-80% of the GPU market share they can do whatever they want because your options are limited. AMD with their 12% market share aren’t much better as it has come out that they were intentionally limiting chip production into 2023 to keep prices high. AMD is still trying to sell the RX7600 at a cost that is unreasonable and sales have been poor as a result. Nvidia seems to be happy about the reduction in sales because they are making vastly more profit per sale. Since Nvidia is in a dominate position they are basically betting that the lack of choice will keep that profit train rolling as they squeeze consumers for more. The only thing that might save the GPU market is intel. It’s kind of terrifying that the only hope for the restoration of reasonable prices is Intel…

When ONE baby formula plant shut down it caused a baby formula supply crises. That’s how few companies are actually involved in the production of baby formula that just ONE of their factories shutting down caused near catastrophic results. Now think about that earlier fact I stated about nearly all the brands in your local grocery store being owned by 1 of 11 companies and tell me how that allows for competition…

When ONE baby formula plant shut down it caused a baby formula supply crises. That’s how few companies are actually involved in the production of baby formula that just ONE of their factories shutting down caused near catastrophic results.

There are plenty of baby formula companies–they’re just not allowed to sell in the US because of protective tariffs and FDA labeling laws–which were allowed to be ignored when the one US company shut down. What happened? European companies stepped up and filled the void.

The lack of competition was deliberately manufactured by the US government in order to “protect” American companies from competition.

@Mu Yixiao: You’re right we should just import whatever from wherever because who cares about some lead or fake baby formula that killed how many children?? Clearly the free market will work that all out or something..

It has zero to do with safety. European baby formulas meet US safety standards (as it shown by the fact that they were allowed in during the emergency).

But… hey. Feel free to jump to conclusions rather than looking at reality.

“FDA regulation of formula is so stringent that most of the stuff that comes out of Europe is illegal to buy here due to technicalities like labeling requirements,” Derek Thompson writes at The Atlantic. Formula may end up on the FDA’s “red list” of products to be seized, The New York Times explains, if it has “labels that are not written in English or do not have all of the required nutrients listed.

“But overall, “it’s clear that the U.S. has basically closed off its market to imports,” Mary Lovely, a senior fellow at the Peterson Institute for International Economics, tells NPR News. “There’s really no reason we should be blocking perfectly nutritional formula coming out of high-quality, sanitary plants in the European Union,” she adds. “There is no reason why we can’t be importing baby formula from Canadian plants, which could very easily be inspected by FDA.”

Safe formula from quality plants in the EU and Canada. They are inspected and approved by their respective governments. These companies would love to get the FDA approval to sell in the US, but they’re not allowed to.

Sure, there are some industries that are overly concentrated, that not proof they create inflation. And for graphics cards, prices for those were very high before the pandemic thanks to mining.

@Mu Yixiao: Alright fine I’ll get into a serious nitty gritty response instead of a generic comment meant to provoke you into thinking some beyond the box you inhabit. I was referencing the spout of poisoned baby formula in a serious manner though as that’s killed a whole slew of kids over the years (particularly in China). This all started when whistleblower complaints were finally taken serious by the FDA at the Abbott Laboratories factory in Michigan. That one factory accounted for 40% of the nation’s supply. Personally I’m fine with shutting down a factory that has a deadly bacterial contamination problem. This closure occurred in February of 2022.

In response Joe Biden on July 2022 waived tariffs on imported formula. As part of this the FDA also relaxed it’s rules/restrictions allowing for european imports to increase dramatically. Safety standards =/= formula content requirements. The EU’s requirements for baby formula’s contents differ in important ways from the FDA’s. Though honestly I see the FDA requirements as more pandering to domestic interests than it should be. A bigger issue in my view is the labeling as it’s hard to know how to mix baby formula when you need google translate to try to understand the instructions. Lets convert metric to imperial and now try to figure out what the fck this spanish means in english. THe lack of warning labels about iron content etc also annoyed the FDA but all of this was relaxed quickly and heavily in response. The Biden administration is still pushing where they can to diversify our supply of baby formula via Europe and Canada (the GOP refuses to help). Fun story but the issue with Canada formula stems from Trump’s USMCA agreement. I really don’t want to go into the details on that so I suggest you use google. I will say I’m more than a bit worried that when the next GOP president is elected that they’ll kill Biden’s expansions because somethingsomethingMURICA!!… Seriously I can already see the talking point about how Biden made us reliant on europeans blahblah antiamerican…

Why do you think European companies are going to manufacture excessive amounts of baby food while domestic USA producers don’t? What unique situation exists for the EU that manufacturers in the USA don’t consider or experience?

@Andy: Mining is only relevant to the story as it created the opening for higher prices to begin with. The point still remains that greedflation is clearly at play despite the claims of the companies/individuals profiting.

Most of our industries are overly concentrated due to a lack of willpower to enforce any of the relevant laws to prevent that from occurring. I’ve already provided proof of that problem existing in multiple industries (the most worrying being our food supply) in the last two posts. At this point I’d like to see one industry where over concentration hasn’t resulted in monopolistic activities.

This analysis ignores something else significant. I will agree that at least some of the inflation had external causes (supply chain interruptions, labor shortages, etc.), and it is difficult to determine what percentage of the increases were from the external causes and what percentage were from sellers padding their profit margins.

However, as the external causes of the inflation surge have been alleviated, prices remained at the higher levels, rather than competition pushing prices back to pre-COVID levels. This is hard to explain, without attributing it to greed. This is suggested by the IMF chart you cite, where the corporate profits portion of inflation increases has grown in the last few quarters, even as supply chain interruptions have lessened.

Rents increased rapidly when people were receiving pandemic money. Now that money is no longer coming in, rents are no longer increasing as much. They’re also not coming down as their tenants income decreases. I doubt landlords are the only business folks who take advantage of opportunities like this to further feather their shareholders’ nests.

The article is pretty ridiculous and admits that corporate profiteering may have led to inflation. But it would be wrong, morally, to make a morality play out of it. Morality is only for the little people, I guess, like the moral hazard of forgiving student loans.

@Moosebreath:

One of the articles Levitz mentions has the chief economist from UBS saying that recent inflation has been driven by profit-seeking. This is just a weird piece about a crude strawman intended to lull people into believing what they’re told.

But, as several of the commenter you quote at least imply, the COVID-related supply shortages had the side effect of increasing the monopoly power of large providers in numerous markets. They couldn’t raise prices before because there were too many competitors who could undercut them — but under COVID those competitors were pushed out of that market (or at least reduced as a significant factor) by supply issues. That’s what changed.

…and as noted by @becca, price elasticity is not symmetric. Prices go up much more quickly than they come down, even if the economy returns to its previous state. It’s a ratchet — it sticks at the current level, and can really only move in one direction barring major recession. Any opportunity to raise prices temporarily becomes permanent.

Reich has been pointing this out for decades, ever since antitrust regulators started accepting the absurd argument that consolidation will actually lower prices because of efficiency. And his premise is correct: highly concentrated industries main reason for not raising prices is concern that consumers will buy less of their products. But once prices have been raised and accepted as the new normal, they have no incentive to lower prices since they have little competitive pressure. Covid provided a reason to ratchet prices up, and there is little competition to bring it back down.

Reich’s analysis is far from faulty. It’s dead on.

I’m reminded of back in 2009, my employer made a significant reduction in what was covered by our health insurance while jacking up what we paid for it, and claimed this was a result of new Obamacare requirements. This made no sense because our employer self-insured and wasn’t even covered by the law.

After complaining about this to someone I knew in HR, they confided that the company was lying because they knew half the employees would believe anything bad that happened healthcare related that was blamed on Obamacare, so it was a great way for the company to reduce the value of benefits and have most of the work force blame someone else for it.

The reason I’m bringing this up now is that I suspect the answer to the “why didn’t the corporations do this before now?” is similar. They’ve discovered that nebulous “supply chain problems” is a great excuse for all kind of things, from inflated prices to crappy service and a big chunk of the public will blame someone else for it.

The problem is that like a lot of regulations, Republican judges have so watered down these laws that it’s nearly impossible to enforce these laws unless a particular company is dumb enough to more or less publicly confess to it.

For example: right now 90% of the commercial landlords in the US use the “asset optimization algorithm” from the same company, RealPage, to “recommend” the rental amounts for their properties. Now by any reasonable definition this should be considered a price-fixing cartel, but since everyone involved claims that’s not their actual motivation, it’s more or less impossible to prosecute.

When you go to your local grocery store pretty much every brand in there is owned by one of eleven corporations…

@Modulo Myself: Hey now! If we start forgiving student loans, how are we going to keep up the number of poor people desperate for work at even low wages that we’ll need to keep wages depressed? It all works together. It’s not two different models and never has been. It’s all factors in one system.

@Stormy Dragon:

I’m reminded of the DISH TV commercial, where the child is selling 6 ounces of lemonade at a sidewalk stand for 5 dollars, and explains that the cost is due to “supply chain problems”.

Or recently my church reported a 50% increase in income from selling perogies (as compared over the past ten years). They didn’t sell any more volume (in fact the volume fell) what they did was increase the price (blaming ingredient increases during the pandemic), to maintain their pre-pandemic margin. Since those costs decreased beginning late summer, they kept the same pricing but effectively saw a 300% increase in their margin.

IMO, what would be revealing in the discussion of inflation is some data on margin.

Can the corporation selling widgets with a 20% margin, justify increasing that margin to 80%?

OTOH, in a capitalistic environment, accumulating evermore wealth is the objective, regardless.

Let me paraphrase: That greed caused inflation is absurd but greed is the natural state of capitalism. Amazingly, these two separate and contradictory thoughts are next to each other. So despite the above, let’s just say that inflation is not clearly understood by economists but it probably has many causes, and yes, greed probably is a contributing factor. Historically, oil prices have been the main driver for inflation, but as stated, many other reasons exist such as surplus capital, tight supply chains, and scarcity. The bottom line is that each element can contribute to inflation and it is usually a combination of factors.

Yup. This graph shows the story.

I think all that’s left is to argue about what happened during that time period that let corporations increase prices without getting hit by consumers fleeing to competitors or cutting back.

If you don’t like ascribing emotional reasons to companies, you could reframe the corporate greed as price resistant markets or something.

@MarkedMan:

Except that inflation has always had a ratchet effect, including prior to the consolidation, Reich talks about.

And if his theory had any merit, we’d see the highest inflation in the industries that have had the most consolidation since the 1980’s – is that what we actually see? Here’s one chart and I don’t see any obvious pattern that would suggest that Reich is correct.

Also, we have constant inflation except when we’re in a recession or depression. Prices increasing by the Fed’s target rate of 2% a year for three years vs 6% for one year are both going to ratchet. Inflation in the 1970’s – before Reich’s consolidation, ratcheted.

So I think Reich is wrong – what we’ve seen over the last couple of years is almost entirely about supply and demand creating inflation, not a few greedy industries creating it.

We had a situation where demand for some things plummeted while it spiked for other things. At the same time, supply was constrained. That is always going to cause prices in significantly increase.

@Andy:

There’s very little in the way of competition in most markets so corporations are extremely reluctant to let go of those extra profits. Look at what Nvidia did for the 40 series of graphics cards (their latest generation). They cost +$200 more than the last gen 30 series versions and provide the same or less performance. This despite TSMC’s yields resulted in a reduced silicon cost. So Nvidia not only are using chips that are cheaper than the prior generation they also cut back on the ram side to save even more money. NVidia pocketed all those savings and decided they wanted to still make hundreds more per card than they did last generation. Since Nvidia has 70-80% of the GPU market share they can do whatever they want because your options are limited. AMD with their 12% market share aren’t much better as it has come out that they were intentionally limiting chip production into 2023 to keep prices high. AMD is still trying to sell the RX7600 at a cost that is unreasonable and sales have been poor as a result. Nvidia seems to be happy about the reduction in sales because they are making vastly more profit per sale. Since Nvidia is in a dominate position they are basically betting that the lack of choice will keep that profit train rolling as they squeeze consumers for more. The only thing that might save the GPU market is intel. It’s kind of terrifying that the only hope for the restoration of reasonable prices is Intel…

When ONE baby formula plant shut down it caused a baby formula supply crises. That’s how few companies are actually involved in the production of baby formula that just ONE of their factories shutting down caused near catastrophic results. Now think about that earlier fact I stated about nearly all the brands in your local grocery store being owned by 1 of 11 companies and tell me how that allows for competition…

@Matt:

There are plenty of baby formula companies–they’re just not allowed to sell in the US because of protective tariffs and FDA labeling laws–which were allowed to be ignored when the one US company shut down. What happened? European companies stepped up and filled the void.

The lack of competition was deliberately manufactured by the US government in order to “protect” American companies from competition.

@Mu Yixiao: You’re right we should just import whatever from wherever because who cares about some lead or fake baby formula that killed how many children?? Clearly the free market will work that all out or something..

@Matt:

It has zero to do with safety. European baby formulas meet US safety standards (as it shown by the fact that they were allowed in during the emergency).

But… hey. Feel free to jump to conclusions rather than looking at reality.

Safe formula from quality plants in the EU and Canada. They are inspected and approved by their respective governments. These companies would love to get the FDA approval to sell in the US, but they’re not allowed to.

@Matt:

Sure, there are some industries that are overly concentrated, that not proof they create inflation. And for graphics cards, prices for those were very high before the pandemic thanks to mining.

@Mu Yixiao: Alright fine I’ll get into a serious nitty gritty response instead of a generic comment meant to provoke you into thinking some beyond the box you inhabit. I was referencing the spout of poisoned baby formula in a serious manner though as that’s killed a whole slew of kids over the years (particularly in China). This all started when whistleblower complaints were finally taken serious by the FDA at the Abbott Laboratories factory in Michigan. That one factory accounted for 40% of the nation’s supply. Personally I’m fine with shutting down a factory that has a deadly bacterial contamination problem. This closure occurred in February of 2022.

In response Joe Biden on July 2022 waived tariffs on imported formula. As part of this the FDA also relaxed it’s rules/restrictions allowing for european imports to increase dramatically. Safety standards =/= formula content requirements. The EU’s requirements for baby formula’s contents differ in important ways from the FDA’s. Though honestly I see the FDA requirements as more pandering to domestic interests than it should be. A bigger issue in my view is the labeling as it’s hard to know how to mix baby formula when you need google translate to try to understand the instructions. Lets convert metric to imperial and now try to figure out what the fck this spanish means in english. THe lack of warning labels about iron content etc also annoyed the FDA but all of this was relaxed quickly and heavily in response. The Biden administration is still pushing where they can to diversify our supply of baby formula via Europe and Canada (the GOP refuses to help). Fun story but the issue with Canada formula stems from Trump’s USMCA agreement. I really don’t want to go into the details on that so I suggest you use google. I will say I’m more than a bit worried that when the next GOP president is elected that they’ll kill Biden’s expansions because somethingsomethingMURICA!!… Seriously I can already see the talking point about how Biden made us reliant on europeans blahblah antiamerican…

Why do you think European companies are going to manufacture excessive amounts of baby food while domestic USA producers don’t? What unique situation exists for the EU that manufacturers in the USA don’t consider or experience?

@Andy: Mining is only relevant to the story as it created the opening for higher prices to begin with. The point still remains that greedflation is clearly at play despite the claims of the companies/individuals profiting.

Most of our industries are overly concentrated due to a lack of willpower to enforce any of the relevant laws to prevent that from occurring. I’ve already provided proof of that problem existing in multiple industries (the most worrying being our food supply) in the last two posts. At this point I’d like to see one industry where over concentration hasn’t resulted in monopolistic activities.