The May Jobs Report: Steady, But Nothing To Write Home About

The jobs news in May was good, but far from great.

Going into May’s jobs report, there were a wide variety of expectations regarding where the economy as a whole actually was, and what that meant for the jobs market. Several economic indicators seemed to suggest that we may have faced a slowdown in May, and the fact that May was also the second full month that the Federal Budget sequester was in effect led many to expect that we’d start seeing a slowdown in hiring in May. Wednesday’s released of the ADP jobs report, which sometimes correlates with the Labor Department’s numbers and sometimes doesn’t, suggested that the labor market was healthier in May than many analysts fear. As it turns out, the BLS report that was released today showed that the jobs market remains steady and healthy, but still nowhere near where it ought to be:

Total nonfarm payroll employment increased by 175,000 in May, and the unemployment rate was essentially unchanged at 7.6 percent, the U.S. Bureau of Labor Statistics reported today. Employment rose in professional and business services, food services and drinking places, and retail trade.

Both the number of unemployed persons, at 11.8 million, and the unemployment rate, at 7.6 percent, were essentially unchanged in May. (See table A-1.)

Among the major worker groups, the unemployment rates for adult men (7.2 percent), adult women (6.5 percent), teenagers (24.5 percent), whites (6.7 percent), blacks (13.5 percent), and Hispanics (9.1 percent) showed little or no change in May. The jobless rate for Asians was 4.3 percent (not seasonally adjusted), little changed from a year earlier. (See tables A-1, A-2, and A-3.)

In May, the number of long-term unemployed (those jobless for 27 weeks or more) was unchanged at 4.4 million. These individuals accounted for 37.3 percent of the unemployed. Over the past 12 months, the number of long-term unemployed has declined by 1.0 million. (See table A-12.)

The civilian labor force rose by 420,000 to 155.7 million in May; however, the labor force participation rate was little changed at 63.4 percent. Over the year, the labor force participation rate has declined by 0.4 percentage point. The employment-population ratio was unchanged in May at 58.6 percent and has shown little movement, on net, over the past year. (See table A-1.)

On the job creation front, which is what really matters, things were good, but not great:

Total nonfarm payroll employment increased by 175,000 in May, with gains in professional and business services, food services and drinking places, and retail trade. Over the prior 12 months, employment growth averaged 172,000 per month. (See table B-1.)

Professional and business services added 57,000 jobs in May. Within this industry, employment continued to trend up in temporary help services (+26,000), computer systems design and related services (+6,000), and architectural and engineering services (+5,000). Employment in professional and business services has grown by 589,000 over the past year.

Within leisure and hospitality, employment in food services and drinking places continued to expand, increasing by 38,000 in May and by 337,000 over the past year.

Retail trade employment increased by 28,000 in May. The industry added an average of 20,000 jobs per month over the prior 12 months. In May, general merchandise stores continued to add jobs (+10,000).

Health care employment continued to trend up in May (+11,000). Job gains in home health care services (+7,000) and outpatient care centers (+4,000) more than offset a loss in hospitals (-6,000). Over the prior 12 months, job growth in health care averaged 24,000 per month.

Within government, federal government employment declined by 14,000 in May. Over the past 3 months, federal government employment has decreased by 45,000.

Employment in other major industries, including mining and logging, construction, manufacturing, wholesale trade, transportation and warehousing, and financial activities, showed little or no change over the month.

There were also revisions to the March and April jobs numbers. March’s numbers were revised upward from a net 138,000 jobs created to a net 142,000 jobs created, while April’s numbers were revised downward from 165,000 net jobs created to 149,000 net jobs created. Compared to previous months this is a fairly modest adjustment, but it is the first one in awhile where there’s been a net downward adjustment, in this case of 12,000 jobs between the two months. Looking at individual job sectors, we can clearly see the impact from the sequester in the Federal Government numbers, and it’s unclear how many of those “job losses” are actually furloughs, but they don’t seem to be having any real impact on the economy as a whole. The most substantial growth seems to be occurring in Professional and Business Services and Retail, although it is somewhat concerning that a substantial part of the growth in the first area seems to be occurring in Temporary Help Services, a development which suggests that we may see the market give back some of these job gains in the coming months. It’s also slightly concerning that construction employment seems to be slowing down despite reports of renewed health in the real estate market.

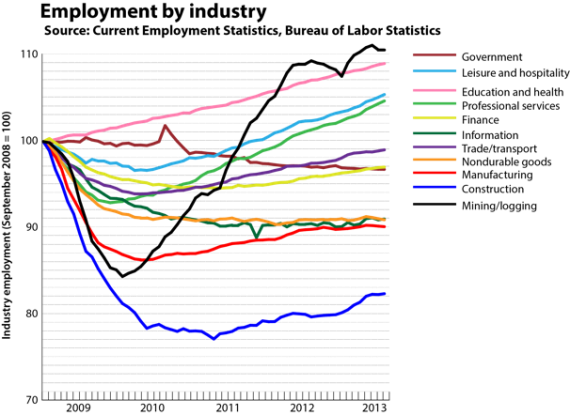

On that note, this chart from Wonkblog provides an interesting look at how various industries have fared both during the Recession, and after it ended:

Interestingly, the industry that has recovered the most quickly is Mining and Logging, although that account for an ever smaller part of the total jobs market. Construction, of course, remains mired in the aftereffects of the Housing Crash. It’s likely to be quite some time before that segment of the economy fully recovers.

It’s not all bad, of course, as CNBC notes, we seem to be avoiding the spring-into-summer slowdown that we’ve experienced in recent years:

Despite anticipation of a spring-into-summer swoon, the U.S. economy continued to create jobs at a relatively steady pace in May, adding 175,000 positions as the unemployment rate ticked higher to 7.6 percent.

Economists expected nonfarm payrolls to grow by 170,000 in the month after an initial reading of 165,000 in April, which was lowered to 149,000.

(…)

“The employment report does not look too bad after all, which should soothe recent concerns over a slowing for the US economy in response to domestic fiscal policy and external headwinds,” Andrew Wilkinson, chief economic strategist at Miller Tabak, said of the report.

(…)

The May payrolls number has been both low and volatile over the past several years, with an average initial reading of 69,000 and an average upward revision of an additional 99,000 positions.

Other jobs numbers had pointed to a slowdown.

The Institute for Supply Manufacturing surveys of both the manufacturing and nonmanufacturing sectors pointed to flat growth, while the ADP/Moody’s Analytics survey of private payrolls earlier this week came in considerably lower than expected.

In other words, May’s jobs report was good, and better than many people expected, but far from great. It was below the level it needs to be at to keep up with population growth, and remains at a rate that would take us until well after Barack Obama is out of office before we’re back at pre-recession employment levels. The report beat expectations, but it’s not too hard to beat expectations when expectations are so low.

Do you have an automatic post generator for when these reports come out?

The [insert month] report on [insert topic] from the [insert government agency] came out this week, and while the news is positive, it isn’t good enough. Here’s a chart.

Look at your chart numbskull….the line that represents Government is the only one that continues downhill.

14,000 Public Sector jobs cut in the month of May.

45,000 Punlic Sector jobs cut in the last three months.

You are getting what you want…why aren’t you cheering????

Doug’s problem is that the conservative economic ideology that Doug is devoted to has been so totally discredited that he can’t really do more than point to the slow economy and complain about it not being better.

According to right wing ideology, deregulated financial markets could not lead to financial crashes because of the Efficient Market Hypothesis. The 2008 crash proved that wrong, and government had to rescue the banks in order to stave off a second Great Depression.

According to right wing ideology, the cure for the financial crash that could not happen is not fiscal stimulus, but austerity. After five years, the verdict is unanimous: austerity made things worse just about everywhere it was tried, and fiscal stimulus either stopped the bleeding or made things better.

According to right wing ideology, what helped in a recession was debt and deficit reduction, and they had the math ( Reinhart-Rogonoff) to prove it. We now know that the math is wrong .

When someone’s ideology has been proven so conclusively wrong, they don’t have much significant to say. It’s obvious now that the liberals have been right all along, and that increased fiscal stimulus is the only way to convert a slow and halting recovery to a vigorous one. But Doug can’t say that, any more than the pope can say that Martin Luther was right. It would be against his religion.

No need to write home. When you can’t find a job and have been out of work for a long time, you probably are already there.

On the “upside” the jobs that are out there are generally 5 days at 6 hours a day and no more. I wonder why?

I guess there is no real estate market in Doug’s world.

Or perhaps a gypsy said she would curse him if he ever talked about it.

So “job creators” like the Walton family can avoid giving their employees benefits, thus passing those costs along to the public, while at the same time adding $$ to their already immense fortunes?

Why on earth would anyone write home about anything? They just like to receive mail from themselves??

Well Doug I realize today’s report doesn’t represent the nirvana you experienced when we were bleeding 750,000 jobs a month but hang in there kiddo!

It’s got to be tough trying to pick out negatives in the news. And it has to cause great consternation to omit things like a quickly recovering real estate sector, reduction in deficits and people starting to look for work again who had given up in the past.

Well, it would cause great consternation to someone with a bit of principle at least.

And no matter what Doug, you’ll always have Bithead and JKB hanging in there with you!

@JKB: Ritzholtz posted a possible answer a few moments ago http://www.ritholtz.com/blog/2013/06/temporary-help-services-reach-record-high/ , that the growth in those positions is a leading indicator of more full time jobs to come.

http://moslereconomics.com/wp-content/graphs/2013/06/NFP.gif

I originally expected a weaker Q2 in the range of 1.8% to 2.2%. I’m now leaning toward that forecast as too optimistic.

Yes, it is bad news that the economic recovery has continued at a slow pace since the financial collapse of 2008. I miss those days when the economy was losing jobs at the rate of 700,000 per month, and the unemployment rate was over 10%.

@rudderpedals:

Temporary workers also can be a canary in the coal mine when it comes to future job losses. If you work at a company that often uses temps, but then they’re gone, it may be a sign of layoffs to come.

@ al-Ameda

39 consecutive months of private sector job creation totally sucks. You seem to have forgotten that late ’08 was a golden age…

@anjin-san:

Those people who thought, and who still believe, that this recession was just another speed bump, and that we’d be over it in 18 months and on way our back to 4% unemployment, are truly delusional.

The crash of 2008 was the worst financial catastrophe since the Great Depression. Nearly $18 Trillion in wealth and income was vaporized in the crash, and millions of jobs were lost in a 7 month run up to Obama’s inauguration in 2009. The fact that we did not go over the cliff into a period of extended recession and, perhaps depression, is due in large part to the economic stimulus (yes, Paul Krugman was, and continues to be, right.)