Projecting China’s Future

Can it overcome demographics and decoupling to sustain its current unprecedented growth?

Via Dave Schuler, I see that Roland Rajah and Alyssa Leng*, two scholars at the Lowi Institute, a well-regarded Australian think tank, predict a far slower rise for China than that which has guided much of US foreign policymaking the last decade-plus.

Their Executive Summary:

The future of China’s ongoing global rise is of great importance to both China and the rest of the world. Predicting long-term economic performance is inherently difficult and open to debate. Nonetheless, we show that substantial long-term growth deceleration is the likely future for China given the legacy effects of its uniquely draconian past population policies, reliance on investment-driven growth, and slowing productivity growth. Even assuming continued broad policy success, our projections suggest growth will slow sharply to roughly 3% a year by 2030 and 2-3% a year on average over the three decades to 2050. Growing faster, up to say 5% a year to 2050, is notionally possible given China remains well below the global productivity frontier. However, we also show that the prospect of doing so is well beyond China’s track record in delivering productivity-enhancing reform, and therefore well beyond its likely trajectory. China also faces considerable downside risks.

Our projections imply a vastly different future compared to the dominant narrative of China’s ongoing global rise. Expectations regarding the rise of China should be substantially revised down compared to most existing economic studies and especially the expectations of those assessing the broader implications of China’s rise for global politics. If China were on track to grow at 4-5% a year to 2050, as many seem to hold, it follows that China would be on course to become the world’s most dominant economy by far. With 2-3% growth, China’s future looks very different. China would still likely become the world’s largest economy. But it would never establish a meaningful lead over the United States and would remain far less prosperous and productive per person than America, even by mid-century.

The report’s Introduction includes these salient points:

China’s ongoing rise will clearly carry enormous implications for both the country itself and the rest of the world. China’s economic prospects are therefore a topic of intense debate. On the one hand, it is well accepted that double-digit growth is a thing of the past and that China faces considerable downside economic risks, including that reform might be stalling and that brewing financial fragilities could eventually trigger a crisis. Several studies argue that China’s economy could soon slow considerably. Nonetheless, most existing studies suggest China can continue to sustain robust growth averaging around 5% a year or higher to 2030. Among studies that attempt to look further ahead, most suggest China could average growth of about 3.5-4% a year over the decades to 2050.

Interestingly, expectations amongst those considering the broader implications of China’s rise for global politics tend to be notably higher at around 5-6% a year sustained to 2050. As the deep determinants of rapid economic growth are both poorly understood and highly dependent on policy and politics, many analysts evidently put a significant weight on recent performance when thinking about China’s future trajectory, essentially extrapolating the trend.

This Analysis focuses on China’s long-term economic outlook to 2030 and further out to 2050. It contends that despite the considerable uncertainties in projecting long-term economic performance, focusing on the basic building blocks or “proximate sources” of future economic growth is sufficient to show that China very likely faces a future of significant structural deceleration, even using relatively optimistic assumptions. Expectations regarding the rise of China should therefore be substantially revised down compared to most existing studies and especially those considering the broader geopolitical implications of China’s global rise.

China’s past population policies mean substantial demographic decline is essentially locked in over the coming decades, with little ability for policy to materially alter the outlook. Economic growth has also been incredibly reliant on capital investment — a model that has become increasingly unsustainable. By our estimate, the growth contribution of capital accumulation will roughly halve over the coming decades compared to that preceding the Covid-19 pandemic. Housing investment is entering structural decline, as urban population growth and increases in average household income both slow. Similarly, China’s ability to rely on infrastructure for growth is close to reaching its limits, after decades of remarkably high investment. While China has more room to rely on business investment to drive future growth, this too has been high and can be expected to run into diminishing returns. Since capital accumulation has accounted for three-quarters of China’s growth in recent years, this has major implications for China’s future economic prospects.

Whether China can sustain rapid economic growth will largely be determined by what happens with productivity growth. Yet Chinese productivity growth has been decelerating, and there are strong reasons to think it will continue to do so — reflecting economic theory, the international evidence, China’s own track record, and the prospect of intensifying “decoupling” from the West. Most contemporary assessments also conclude that overall progress with key economic reforms has been mixed at best. Moreover, even if China can reverse its decelerating productivity trend, history suggests there are limits as to what can realistically be achieved, and therefore limits as to how fast China’s economy can sustainably grow even in a best-case scenario.

Pulling these pieces together using several alternative growth accounting approaches, we show that annual average Chinese economic growth can be expected to decelerate sharply to roughly 3% by 2030 and 2% by 2040, compared to the pre-Covid trend of a little over 6%. Over the almost three decades from 2021 to 2050, economic growth would average about 2-3% a year. Growing faster, up to say 5% a year, is notionally possible given China remains well below the global productivity frontier. Nonetheless, we also show that the prospect of doing so is well beyond China’s track record of delivering productivity-enhancing reform, and therefore well beyond its likely trajectory.

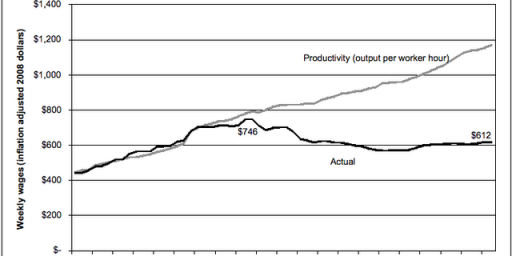

There’s a whole lot more to the report, which is helpfully quite jargon-free and illustrated with numerous charts and graphs.

I’m neither a China scholar nor an economist, so I have very little to add to their analysis or standing for preferring their conclusions over those of other researchers. Because it’s in line with my longstanding sense of the situation, I find it quite plausible but, as they say, predictions are hard, especially about the future.

The number of intervening variables makes predicting national economic trajectories a decade—much less three or four decades—out a mug’s game. I’m old enough to remember when Japan, not China, was set to overtake the United States economically. Events have an annoying propensity to get in the way.

At the same time, as I have said about phenomena such as the various Global Trends reports, long-term forecasting is both impossible and necessary. In the Defense realm alone, we need to make force planning and acquisitions decisions decades out, even while we constantly adjust based on new insights.

Alas, all of the incentives point in the direction of continuing to believe the worst-case projections. While there are great costs to being wrong in either direction, our institutional incentives are much more tolerant of being wrong on the side of over- than under-preparation. China is the most plausible “peer competitor” and serves as a useful “pacing threat” for force development. And, despite at least six decades’ worth of evidence to the contrary, we continue to believe that, if we’re ready for the most dangerous fight, we can handle anything short of that.

___________

*I see from her LinkedIn that Leng moved on to Australia National University’s Development Policy Centre a few weeks ago.

One of the advantages the US has over China that is often ignored is geography. We have direct access to both major oceans through numerous ports. And we have secure borders with friends on both sides. China has access to the Pacific, but only through chokepoints controlled by the US and its allies.

A second advantage is that the US can increase its labor supply simply by opening the door. We’re good at absorbing immigrants, China is not. And it’s not just manual labor, when brains drain they drain into the US, into our superior universities and into entrepreneurship.

A third advantage is cultural. English is, so to speak, the ‘reserve language’ of trade, banking, etc… Our cultural products travel better because English is much more widely spoken, and because we’ve defined cultural norms in force throughout much of the world. We’re also rather better at diplomacy which is a bit amazing but evidently true.

Finally, we have a (barely) functioning democracy which, over the long term, will outperform autocracies.

If we can keep our shit together in our domestic politics we are likely to remain the world’s only true superpower for decades to come.

@Michael Reynolds: I agree with all of that. Americans, including my students, often lament the long-term planning and policy stability advantages of the PRC and other autocrats without taking into consideration the huge downsides that come with that.

And, yes, even though we go through episodes of xenophobia, we still absorb young talent from abroad phenomenally well. It’s a massive competitive advantage that elites of both parties have traditionally understood. It’s a shame that the GOP is currently working against our interests on that front.

@James Joyner: You might assign your students some Hayek. Could one make a case that the accelerated economic growth in China of the last twenty years was due to relaxation of central planning?

@Slugger: My impression is that is true, but not in the way that you might think. The five year plans are still drive changes to the economy and the standard of living. For example, the goal to raise the health insurance status of 400M Chinese citizens by one notch in a five year period was something that could only work if dictated from Beijing. But each province was given a great deal of latitude on how it was achieved. My understanding is that provinces have an informal divvying up of things to focus on, and at the end of year 2 they look to see what appears to be moving the needle and adapt that themselves. So only the “central” part of central planning has been relaxed.

If you mean the spread of capitalism or “socialism with Chinese characteristics”, that goes back to the late 80’s.

Too true. How much will China’s aging demographic be offset by automation and AI? How much will their deeply racist belief system, which prevents them from seeing any other people as allies or partners, frustrate their ambition to control the Pacific? How many of the next generation of movers and shakers will be driven to emigrate by Xi’s crackdown on society?

@Slugger: Considering Hayek would seem to demonstrate that one can make an argument for anything one believes in firmly enough, but that was mean of me to say.

@Just nutha ignint cracker: I have thought about Hayek a lot. Selma, of course, not Friedrich. He does make valid points about the problems of top-down central planning, and he should not be held responsible for some of the people who claim his ideas. Did you know that Selma and Penelope Cruz shared an apartment in NYC when both were young actors?

@Slugger: this is a much richer topic, and I think a lot of charts and graphs might be in order.