July Jobs Report Not A Home Run, But Still Pretty Good

While not as big as previous months, the July Jobs Report was still mostly good news.

Heading into today’s release of the July employment report from the Bureau of Labor Statistics, analysts were expecting a slightly less spectacular month that we had seen in May and June when we saw very strong job growth even in the face of disappointing reports about economic growth in the first three months of the year. Roughly speaking, the consensus going into the morning was that the unemployment rate would remain steady and that we’d see roughly 230,000 jobs created. As it turns out, the numbers were actually a little below those estimates, but still fairly good and indicative of a positive, albeit not very strong, trend:

Total nonfarm payroll employment increased by 209,000 in July, and the unemployment rate was little changed at 6.2 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in professional and business services, manufacturing, retail trade, and construction.

Both the unemployment rate (6.2 percent) and the number of unemployed persons (9.7 million) changed little in July. Over the past 12 months, the unemployment rate and the number of unemployed persons have declined by 1.1 percentage points and 1.7 million, respectively. (See table A-1.)

(…)

Total nonfarm payroll employment increased by 209,000 in July, the same as its average monthly gain over the prior 12 months. In July, employment grew in professional and business services, manufacturing, retail trade, and construction. (See table B-1.)

Professional and business services added 47,000 jobs in July and has added 648,000 jobs over the past 12 months. In July, employment continued to trend up across much of the industry, including a gain of 9,000 jobs in architectural and engineering services. Employment in temporary help services changed little over the month.

Manufacturing added 28,000 jobs in July. Job gains occurred in motor vehicles and parts (+15,000) and in furniture and related products (+3,000). Over the prior 12 months, manufacturing had added an average of 12,000 jobs per month, primarily in durable goods industries.

In July, retail trade employment rose by 27,000. Employment continued to trend up in automobile dealers, food and beverage stores, and general merchandise stores. Over the past year, retail trade has added 298,000 jobs.

Employment in construction increased by 22,000 in July. Within the industry, employment continued to trend up in residential building and in residential specialty trade contractors. Over the year, construction has added 211,000 jobs.

Social assistance added 18,000 jobs over the month and 110,000 over the year. (The social assistance industry includes child day care and services for the elderly and persons with disabilities.) Employment in health care changed little over the month, with job gains in ambulatory health care services (+21,000) largely offset by losses in hospitals (-7,000) and nursing care facilities (-6,000).

Mining added 8,000 jobs in July, with the bulk of the increase occurring in support activities for mining (+6,000). Over the year, mining employment has risen by 46,000.

Employment in leisure and hospitality changed little in July but has added 375,000 jobs over the year, primarily in food services and drinking places.

Employment in other major industries, including wholesale trade, transportation and warehousing, information, financial activities, and government, showed little change in July.

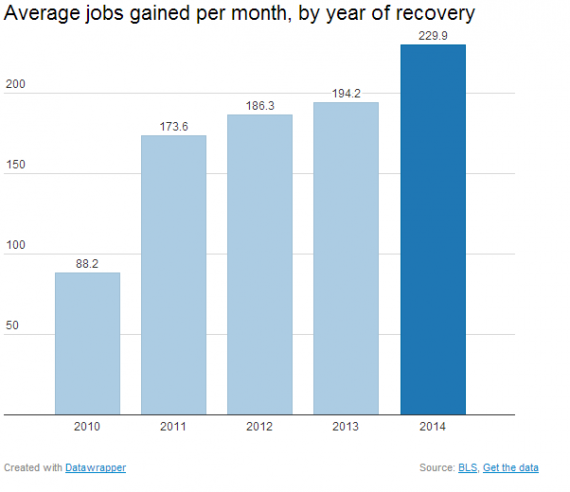

Revisions for the previous two months were minimal, but positive. Net job growth in May was revised upward from 224,000 to 229,000, and June’s numbers were revised upward from 288,000 to 298,000. While this month’s numbers aren’t on the level of these previous months, at least not until we see revisions in September and October, this is the sixth straight month in which we have seen job growth above 200,000 net jobs per month. Additionally, for the first seven months of the year we have averaged roughly 229,828 new jobs created per month. For the past three months, we’ve averaged roughly 245,000 net new jobs per month. This is the strongest average job growth we’ve seen for the entire recovery. In 2010, for example we averaged 88,000 net new jobs per month. In 2011, that number rose t0 173,000 jobs per month, then 186,000 per month in 2012, and 194,000 per month in 2013. As Derek Thompson notes today at The Atlantic, so far 2014 has been the best year for job growth since the Great Recession, and that is an unqualified good thing, as this chart shows:

Looking deeper in to the report, there are still signs that the lingering effects of the jobs recession have yet to be healed, but still plenty of good signs. The abor force participating rate and total employment rates remain at rates unseen since the early 1980s, for example, and the long term unemployed still account for nearly one-third of the labor force. At the same time, average hourly earnings increased again last month, people working part-time for “economic reasons” decreased significantly, and the main reason that the U-3 unemployment rate increased was because of a large increase in the number of people seeking work, which is generally seen as a positive thing since it is indicative of the fact that people believe there are jobs worth looking for.

The New York Times notes that the report shows continued growth, albeit at a slower pace:

The economy continued to advance at a healthy pace in July, creating 209,000 jobs and adding to a string of positive economic news in recent weeks that suggests it is gaining strength after years of lackluster growth following the recession.

But the job gains were lower than in prior months and less than Wall Street had expected, perhaps helping to calm fears that the economy is accelerating too quickly.

The Labor Department said Friday that unemployment increased to 6.2 percent. Economists had been expecting the unemployment rate to hold steady at 6.1 percent. On the jobs numbers, the consensus among economists was an expectation of about 230,000 new jobs.

The number of jobs added last month was well below the revised 298,000 surge reported in June. The average monthly gain in payrolls has been above 200,000 for the last six months, a healthy pace of job creation.

“The job market is kicking into a higher gear; that’s been the story line since the start of the year,” Mark Zandi, chief economist for Moody’s Economics, said in a telephone interview before the Labor Department’s release. “We’re gaining traction.”

Such optimism was supported on Wednesday when the Commerce Department, in its initial estimate of the economy’s overall output for April, May and June, reported that the gross domestic product grew at a seasonally adjusted annual rate of 4 percent for the quarter, surpassing expectations, rebounding from a 2.1 percent decline during the harsh winter quarter.

CNBC had a similar take:

The U.S. economy created 209,000 jobs in June, below expectations, as the unemployment rate climbed to 6.2 percent, reflecting a consistent but unspectacular level of employment growth.

Economists expected nonfarm payroll growth to hit 233,000 in July, down from an upwardly revised 298,000 in June, and unemployment to fall to 6.0 percent from 6.1 percent. An alternative measure of unemployment which includes the discouraged and those working part-time for economic reasons—the underemployed—rose slightly to 12.2 percent.

Traders liked the unemployment data, perhaps intuiting that it would keep the Federal Reserve on hold with its ultra-easy monetary policy. Stock futures had been under selling pressure earlier after Thursday’s aggressive selloff

“That stocks should rise on the relief of a weaker than expected reading, possibly because it is a bond friendly report, suggests investors are clutching at the safety net of easier for longer Fed policy,” said Andrew Wilkinson, chief market analyst at Interactive Brokers. “However, the basis of Thursday’s worst day of the year was probably less centered on falling bond prices and had more to do with geopolitics and global equity price weakness. It all seems rather odd that stock futures have just about eliminated a double-digit slide ahead of the number.”

Market experts said the numbers were right around the sweet spot that reflected economic growth that was solid but not strong enough to change the central bank’s approach.

“It is calming fears of more aggressive hawkish Fed behavior,” said Lawrence Creatura, portfolio manager at Federated Investors. “‘Goldilocks’ is a cliche that’s been beaten to death, however, the cliche fits and this is a data points which supports the not-too-hot not-too-cold pattern of economic data.”

On the whole, while not as spectacular as the previous two months, this is a decent jobs report that indicates that trends are continuing to move in the right direction. Hopefully, things will only get better.

I’m not so sure. The real story is part time jobs and incomes.

The month saw a decline of 142k in jobs in the 24-55 demo, with all gains in the older set and very young. That will inevitably translate into a part time jobs story. This is no different that the 289 net from last month.

All jobs are not created equal.

@Guarneri: Correct.

so, the question becomes, good as compared to what, exactly?

@Eric Florack:

Good compared to the nightmare at the end of the last administration.

I don’t see anything that changes my basic “muddling through” assessment.

And why would it? It’s not like we’ve done anything significant. We did a stop-gap stimulus and that was it. But we had both the immediate crisis and long-standing problems. We (inadequately) addressed the former, but really haven’t done much of anything about the latter. So the same basic problem we’ve had for ~30 years now (productivity growth doesn’t translate into real wage growth except for the top ~10% of the population, with it skewed heavily towards a fraction of the top 1%) continues. Median (real) household net worth continues to fall or at best hold steady over time, placing increased strain on middle & working class budgets, which either leads to reduced consumption (less demand) or people taking on more debt, which has negative consequences as well.

Short version: a large chunk of the country is tapped out and can’t realistically spend more. Household debt overhang is still significant.

Unless we manage to transform ourselves into an export economy (status quo = the inverse), where exactly is increased wealth (per capita) supposed to come from? Said transformation doesn’t really look plausible to me. We really went all-in on free trade and offshoring. Now what?

Rob

Let’s stipulate that all you say about structural problems is true. Do you a) adopt policies that get in the way or b) adopt policies that minimize impediments.

This administration desires more taxes, higher cost to employ, subsidizes losing enterprises such as GM or solar, fights all things fossil fuel, implements a health care law that is driving part time employment…….

It has adopted the former, and wonders why incomes and employment lag, and GDP muddles through.

Erik

Compared to France, apparently.

@Eric Florack:

Good compared to the loss of 700,000 jobs monthly that resulted from the financial crash that the previous administration left us with.

@Guarneri:

We see different things “getting in the way.”

And of course there are other priorities too. Even if “drill baby drill” was a serious policy (it is not, as the effect of lifting restrictions that exist would be small), it would be a very short-sighted policy. Climate change mitigation is often framed as “costing too much.” The thing is that climate change resutling from continuation of the status quo would cost much, much more.

Regarding taxation: a staggering amount of the nation’s total wealth is held be a small number of people. They only need so many houses, appliances, cars, etc. This, in my opinion, is part of the demand shortfall. If that money was spread out more, demand would rise, even absent other factors. The administration has pushed for (and to an extent gotten) high-end taxes, not a general tax increase. In fact, one important part of the stimulus package was the temporary payroll tax cut – the most stimulative tax cut I can think of, really. Unfortunately, that cut was not extended (where was the GOP on that? My recollection is that they wanted that to expire).

More importantly, I think all of the things you list are tiny factors at the margin. None of them are big deals. The income tax increase that was passed was small and hits only a small # of people. The taxes included in the ACA are likewise small potatoes. That’s it for taxes. Federal drilling restrictions are not holding the economy back. I understand that this is a shibboleth on the Right, but we simply don’t have the reserves necessary to become a petro state.

Re: part-time employment, last I checked that was something that has been increasing for a long time, certainly pre-dating the ACA. I understand that it’s politically convenient to try and tie every bad trend to something your opponent has recently done, but it doesn’t actually check out (for the record, I do not blame Bush for the 2008 financial crisis. The structural damage was done, IMO, in the 1980s and 90s, and I place more blame on Greenspan – who chaired the fed for forever – and various Congresscritters of both parties, than I do on the Bush admin).

Here’s my basic analysis:

For ~35 years, real wage growth has not tracked productivity. The profits that came from greater productivity have accrued to (skimmed by) the folks at the very top. There are various reasons for this, but I think the #1 reason is the mobility of capital + the availability of cheap labor overseas + advances in shipping (containers). Throughout this period, we pursued a policy of liberalizing international trade. I understand why – theoretically, the overall impact should be positive. But the distribution, ah, that’s another thing. A few make out great and thousands took it on the chin. Redistribution in our system mitigated this somewhat, but not entirely. It builds for decades. Meanwhile, in the 90s and 2000s, interest rates were nice and low, making it relatively easy for households to load up on debt and thus paper over the problem. The housing bubble exacerbated this terribly – inflating household net worth (which is mostly held in the form of one’s house) for lots of people. Then the music stopped, and here we are, dealing with the aftermath.

To me, the problems go back to the mid-1970s and are thus difficult to pin solely on one party. I don’t think Reaganomics helped matters, at all, but neither do I think they were The Reason we’re having trouble today. I think global trends are dominant, with government policy playing a secondary role. As you note, bad policy (e.g., supply-side economics) doesn’t help.

@Guarneri:

Well, that raises a question: which developed countries came out of the 2008-2009 crash better than we have, and how did they manage it?

A commentor over at Kevin Drum’s blog posted this:

Now obviously I’m taking it back beyond 2000, but this is what I’m saying. We had a terrible recovery from the recession of 2000-2001 too, it’s just that the 2008-2009 crash was bigger. The recoveries look very, very similar to me.

I think that we basically lived on borrowed time in the 80s and 90s. Household debt levels have been steadily increasing since the end of WWII. Once real wage growth decoupled from productivity growth in the mid-70s, that set up a timebomb. We could only paper it over for so long. 2000 was a shock but we basically didn’t get the message. 2008 smacked us in the face with reality so hard we couldn’t ignore it anymore. Now things look terrible to us, because a lot of our past experience was built on pixie dust.

So, what now? I mean that seriously. I don’t know what policy changes would work. Though I am now critical of the full-on free trade/outsourcing policy approach, I’m really not sure attempting protectionism would’ve been any better (indeed, it could have been worse). I simply don’t see a way of keeping capital and super cheap labor apart. Heck, if it hadn’t been for the 2nd world, this all would probably have happened sooner.

@Guarneri:

One of the saddest results of the Obama Administration ‘s inadequate stimulus is that conservatives like you get to continue in your misguideded beliefs. OK, Krugtron again, but only because, as usual , he is right. He has pointed out that most economists are in complete agreement about stimulus:

I’m sure you have been getting your info from Fox News, so of course you KNOW that the stimulus was a failure. But of course, most economists know you are dead wrong.

A great example of how conservative economics doesn’t work is Kansas.

So much for conservative economics! And when we look abroad, Europe imposed the same kind of austerity economics the conservatives suggested-and they are deeper in recession than we are.

Are there any statistics on summer jobs? I know some students who have been trying to find a summer job. Time is running out for this summer.

@Rob in CT:

Well, there is no doubt at all that the European countries that imposed austerity are doing worse than the US.

One country that did well after the 2008 recession was China:

So that’s pretty good evidence that stimulus and Keynesian policies work. But conservatives have always been good at ignoring evidence in favor of ideology.

Ah yes, Krugman, Fox News etc.

No wonder I quit posting here.

I take it back. You are all correct. The economy is roaring. Incomes rising. Business investment sizzling. Consumer debt loads declining. Employment is sparkling. The nations finances improving and if you want to keep your doctor, you can………with lower premiums. How silly of me to not realize all this.

Your comments make good stuff for an internet site, but out in the real world all those struggling people are wondering where that “summer of recovery” went. I have the answer: Fox News reported bad statistics and the recovery fizzled…..”unexpectedly.”

Back to your little check mark game.

@ Guarneri

I’m not sure what you are complaining about. We are getting the economy conservatives wanted. The rich are getting richer. A lot richer. Everyone else is left to fight for the crumbs.

@Guarneri:

Indeed the economy is recovering, albeit slower than it should be( mostly because of misguided Congressional Republican obstruction) . The stock market, for example, IS booming. But go ahead and ignore all that. I’m sure the comforts of conservative dogma are superior to facing actual reality.

@Guarneri:

Can you cite an example of any political movement anywhere in the world in the last 30 years that tried option “b) adopt policies that minimize impediments” which in turn led to “The economy is roaring. Incomes rising. Business investment sizzling. Consumer debt loads declining. Employment is sparkling.”? Bonus points if the impediment minimizing policies strengthened the middle class.

You and stonetools both acknowledge that the recovery has been weak and continues to be so. You contend this is because government policies got in the way and stonetools contends it is because government policy didn’t stimulate enough. stonetools has offered up some empirical evidence to back up his position (granted imperfectly, since less austerity doesn’t exactly equal more stimulus and state level tax cuts don’t exactly equal national laissez faire governance). Do you have even imperfect examples that demonstrate the efficacy of the policies you prefer or is yours a theory that will always prove true because it’s never truly tested?

To my eye while the number of new jobs is still, frankly, too small to bring those who lost their jobs in the Great Recession back to work, the number of sectors seeing job growth is encouraging.

@Rob in CT:

To your factors I would add currency manipulation. (Again to my eye) the empirical evidence is that fiscal stimulus has been buoyed by a very small Keynesian multiplier and that’s largely because the additional spending and hiring our stimulus produces takes place in China because we import too darned much.

I don’t think that our policy-makers have caught up with the differences between today’s economy and that of the the U. S. in the 1930s.

Subtract the housing bubble and we haven’t had much job creation in decades. Neither has anyone else in the developed world.

1) Globalization.

2) Technology.

As Rob in CT points out, there’s no reason to suppose that protectionism would have worked any better.

If you give a bunch of jobs to foreigners and another bunch of jobs to machines you end up with fewer jobs. It’s magical thinking to assume we’d somehow end up with as many or more jobs. There are simply hundreds of billets that are now essentially owned by foreigners or machines. It is a global phenomenon, no one knows what to do about it anywhere, not the French, the Brits, the Germans, the Japanese or us.

There is no “fix.” We do not have the ability to somehow manipulate the global economy from Washington. There is only adaptation.

Heh … I know what to do, take the money that has disproportionately gone to the mega rich and funnel it back into the economy. It’s about time to consider a guaranteed minimum income. This will be paid for by a much more progressive tax system (eliminating corporate loopholes of course) and bang problem solved. Don’t thank me.